Why Poor Credit Can Triple Your Homeowners Insurance

It’s no secret that credit scores play an increasingly important role in our financial lives, determining everything from whether we qualify for a mortgage to what interest rate we’ll get on a new credit card. What still may surprise some, however, is how significant credit scores are in determining what we pay for homeowners insurance.

For the third consecutive year, a Quadrant Information Services study, commissioned by insuranceQuotes, examined the average impact your credit-based insurance score has on what you pay for home insurance — and the numbers are more revealing than ever.

The study found that if you have a fair (i.e. median) credit score, you may pay 36 percent more for home insurance than someone with excellent credit. That’s up from a 32 percent increase in 2015 and 29 percent in 2014.

What’s more, if you have poor rather than excellent credit, your premium more than doubles, increasing by an average of 114 percent (up from 100 percent in 2015 and 91 percent in 2014).

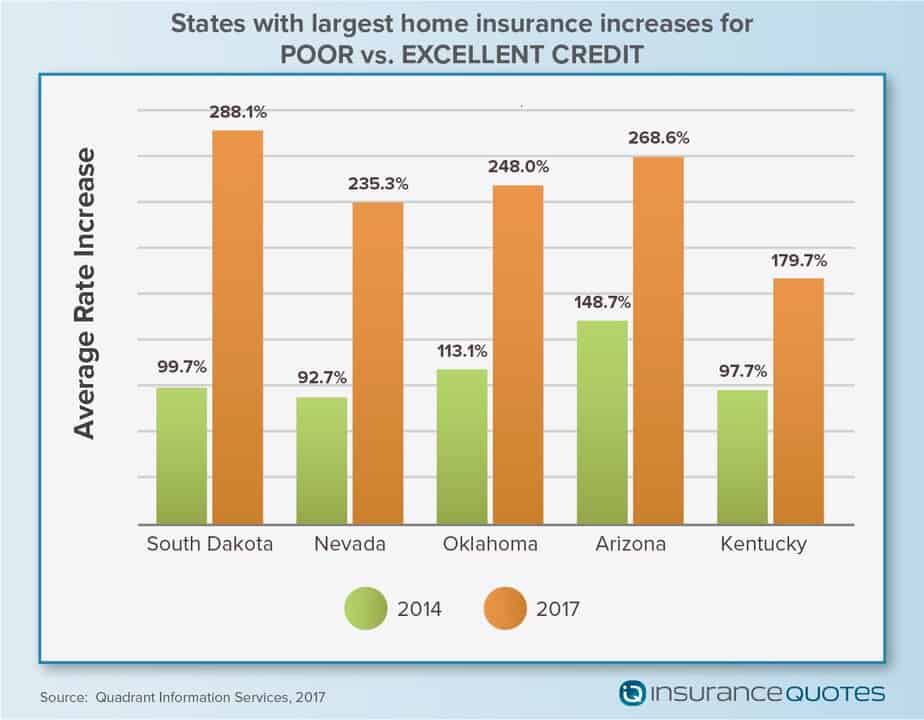

As in years past, premium swings were more dramatic in certain states. For instance, South Dakota homeowners with poor credit-based insurance scores will pay an average of 288 percent more for home insurance than someone with an excellent score in that state (the largest price difference to date).

Meanwhile, other states showed that a credit-based insurance score will play a less significant roll in determining annual premiums. For instance, Florida homeowners with a poor credit-based insurance score will only pay an average of 26 percent more for home insurance than someone with an excellent score in that state.

Here are ways insurers use credit history and how you can improve your score and potentially pay less for home insurance.

What is a credit-based insurance score?

No one has a single, all-encompassing credit score. You’ve got dozens, actually, and each one is used differently depending on the financial circumstance.

For instance, you’ve got credit scores that measure your creditworthiness when applying for a new credit card. You’ve got other credit scores used to determine whether you should be approved for a mortgage. And yes, you’ve even got credit scores that insurance companies use to help determine what you will pay for homeowners insurance.

Known as your credit-based insurance score, this figure is derived from a combination of factors in your credit reports and is used to help insurers better determine the likelihood you will file a future claim.

Lamont Boyd, insurance underwriting expert at FICO, says about 95 percent of U.S. home insurers use credit-based insurance scores in states where it’s allowed. (Only California, Maryland and Massachusetts ban the use of credit in setting home insurance rates.)

“Credit-based insurance scores are used by almost every insurance company in the nation because it’s a very good segmentation tool,” Boyd says. “It’s such a powerful tool because it is very, very predictive of future losses. In other words, lower scoring individuals typically have more insurance losses than those in the higher ranges, which means they are more expensive to insure.”

How insurers calculate your credit-based insurance score

It’s important to note that insurance companies uses credit-based insurance score data in different ways. As a result, your credit history may play a more significant role with Insurer A than it does with Insurer B.

Regardless of how it’s used, your credit-based insurance report is created using financial data collected by the three major credit bureaus (Equifax, Experian and TransUnion). The data may include:

- Outstanding debt.

- Length of credit history.

- Late payments.

- Collections.

- Bankruptcies.

- New applications for credit.

Looking back at past insuranceQuotes studies, it would appear that insurers are placing an increasingly greater emphasis on credit-based insurance scores in setting homeowner premiums. In 2014, for instance, Americans with a fair score were paying just 29 percent more — on average — for home insurance than someone with an excellent score.

For consumers with a poor credit-based insurance score, the premium implications have become even more significant. In 2014 they were paying, on average, 91 percent more than those with an excellent score. That difference has since increased, on average, by 23 percent.

“I don’t think anything in particular has changed other than the fact that more and more insurance company actuaries are better understanding the value of a credit-based insurance score in determining the overall pricing of homeowners’ policies,” Boyd says. “The bottom line though is this — if credit-based insurance scores weren’t predictive in helping insurance companies be more competitive, they wouldn’t be using them.”

Credit-based insurance scores and home insurance by state

In our study, we reviewed three tiers of credit: excellent, fair and poor. How these tiers impact your insurance premium varies widely from state to state.

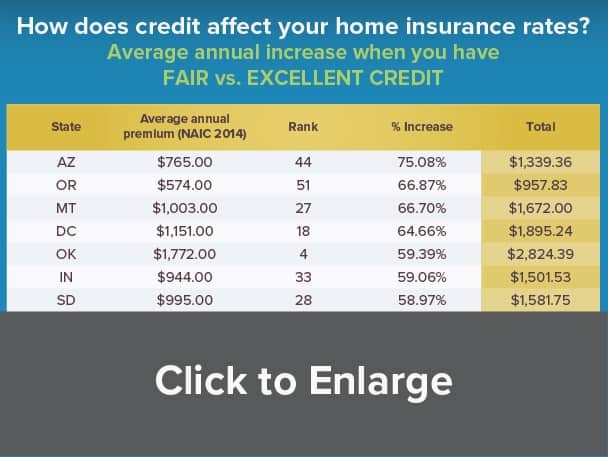

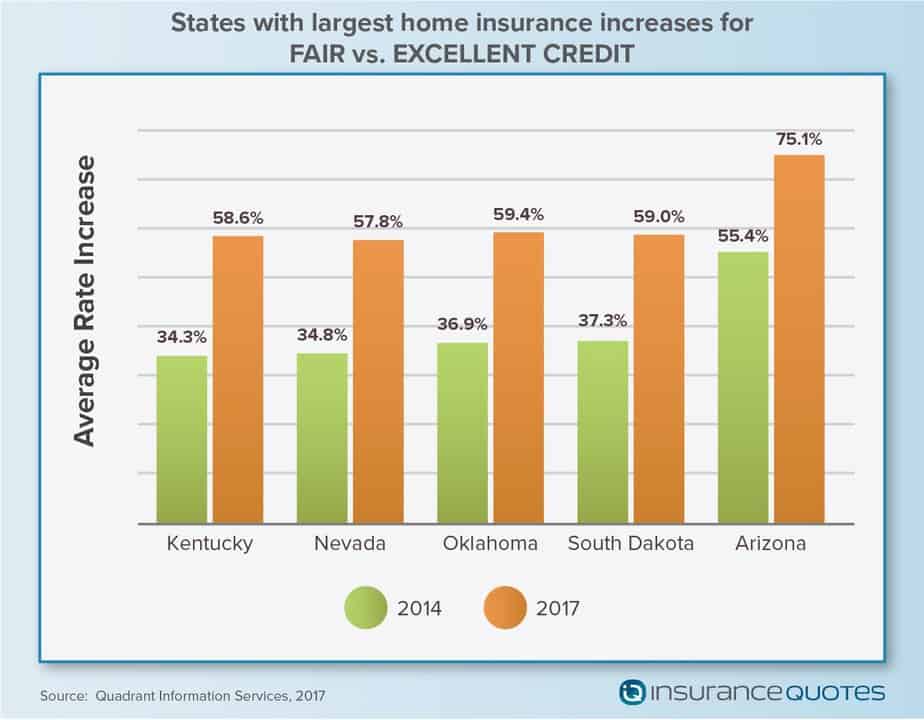

The following five states showed the greatest average premium increase if you have fair credit as opposed to excellent credit:

- Arizona — 75 percent increase

- Oregon — 67 percent

- Montana — 67 percent

- Washington, D.C. — 65 percent

- Oklahoma — 59 percent

Excluding Maryland, Massachusetts and California, the following five states, on average, showed the smallest percentage increase:

- North Carolina — 0.2 percent increase

- New York — 8 percent

- Florida — 10 percent

- Wyoming — 13 percent

- Hawaii — 23 percent

Boyd says these differences come down to the specific ways certain insurers use credit-based insurance scoring to price homeowner policies in a given state.

“One insurance company may want to be more competitive in, say, Oklahoma than they are in, say, Kansas. So they’re going to apply credit-based insurance scores differently in one state over another,” Boyd says.

“That’s why you see such a dramatic difference from state to state.”

The premium increase you see when your credit drops from excellent to poor is even more dramatic. Here are the top five states with the biggest increases:

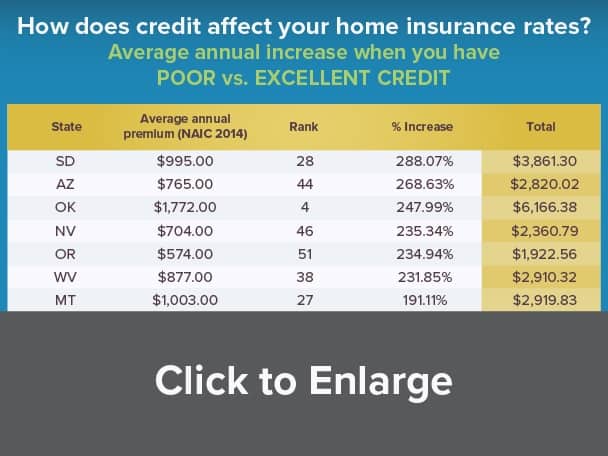

- South Dakota — 288 percent increase

- Arizona — 269 percent

- Oklahoma — 248 percent

- Nevada — 235.3 percent

- Oregon — 234.9 percent

Excluding Maryland, Massachusetts and California, the following five states, on average, showed the smallest percentage premium increase between excellent and poor credit scores:

- North Carolina — 0.2 percent increase

- Florida — 26 percent increase

- New York — 29 percent

- Wyoming — 44 percent

- Hawaii — 53 percent

Again, Boyd indicates that these state-by-state differences indicate “the competitive nature of the insurance marketplace.”

“Insurance companies want to write as much business as they can, and it’s clear to me that in certain states they want to be more careful about how they price various risks,” Boyd says.

Broadly speaking, the data indicates that credit is becoming an increasingly important rating factor in a majority of states, especially for homeowners with poor credit.

Consider, for instance, that in 2015 only one state showed a premium increase of more than 200 percent for those with poor versus excellent credit. This year six states show a premium difference of more than 200 percent for the same comparison, with both South Dakota and Arizona cresting above 250 percent.

What’s more, a poor insurance-based credit score is going to result in consumers paying at least twice as much — on average — as those with excellent credit in all but nine states.

Resistance to credit-based insurance scores

Even though industry experts like Boyd tout credit-based insurance scoring as a powerful predictive tool for setting homeowner premiums, there are many vocal opponents of the practice who claim it’s unfair to consumers, especially those in lower socio-economic demographics.

“This study shows that there is a very dramatic economic downside for people who have credit that’s anything less than excellent, and that seems inherently unfair,” says Amy Bach, executive director of the San Francisco-based nonprofit United Policyholders, a consumer advocacy organization. “They keep telling us this data is predictive but they don’t know why. And as long as they keep showing that it’s predictive they win and consumers lose.”

CHECK OUT: Ultimate Guide to Marijuana Use and Insurance

Because there’s no uniformity or standardization to how this data is used, some insurers weigh credit-based insurance scores very heavily while others may not consider it as important in setting a premium. And this, says Bach, makes comparison shopping very challenging.

“If you ask your insurance agent how they calculate your insurance-based credit score in figuring out your homeowner premium he’s not going to have any idea,” Bach says. “Nine times out of 10 they won’t have a clue what that algorithm is, which means the consumer is at a loss for making comparative market decisions.”

Furthermore, Boyd says Americans have no way of ever seeing their credit-based insurance score. That means consumers shopping for homeowners insurance don’t have access to their credit-based insurance scores the same way they have access to credit scores related to applying for a new credit card or auto loan.

“We have not yet pulled the trigger to put insurance scores on the MyFico.com site,” Boyd says. “A consumer can look at a variety of scores but we have not yet placed insurance scores up there. But generally speaking people with higher credit scores will also be higher in scoring for insurance.”

This imprecision and lack of access to information makes Bach that much more skeptical of the impact credit currently has on home insurance premiums.

“It’s a mystery to me why insurance companies can’t see the ethics problem here. Okay, credit history is predictive. Fine. Put it into the mix a little bit,” Bach says. “But the fact that it clearly has so much weight in setting prices is just unfair.”

How to improve your credit-based insurance score

Boyd says consumers can help improve their credit-based insurance scores the same way they can help improve their overall credit score. A few tips include:

- Pay all of your credit card debts on time.

- Don’t open any new credit accounts unless you absolutely need to.

- Keep credit card balances as low as possible. And if you do have a credit card balance, make sure your balance is less than 30 percent of your credit limit.

Methodology:

insuranceQuotes commissioned Quadrant Information Services to calculate home insurance rates using data from six major carriers with approximately 60 percent market share in each state. The averages are based on a 45-year-old who owns an 1,800 square foot, 2-story, single family home, built in 1976, with $140,000 dwelling coverage, $300,000 liability coverage and a $500 deductible. The three tiers of credit-based insurance scores analyzed were excellent, fair and poor.