Will Adding a Teen Driver to Your Auto Insurance Policy Increase Rates?

Auto insurers are primarily interested in one thing: Are you a safe driver or a risky one? The answer to that question is going to be the most important factor in determining what you pay each year for your policy. The safer (and more experienced) you are behind the wheel, the cheaper a new insurance policy will be.

Conversely, riskier (and less experienced) drivers are going to pay more, and that’s why adding a teen driver to an existing auto policy costs quite a bit − as in 82 percent more.

For the sixth consecutive year, a Quadrant Information Services study – an authority on car insurance cost data analysis – examined the economic impact of adding a driver between the ages of 16 and 19 to a family’s existing car insurance policy, and the numbers were predictably unambiguous: Adding a single teen driver to an adult’s auto policy results in an average annual premium increase of 82 percent.

“Besides driving history, two factors that have a large part in determining and comparing costs on auto insurance rates are your gender and age,” says personal finance expert Natasha Rachel Smith. “Age has the biggest impact on your rate since young drivers with no experience have statistically shown to be more immature behind the wheel. And that leads to more insurance claims, making them much more expensive to insure. In other words, the younger the driver the higher the rate.”

It’s demonstrably true that teen drivers are the riskiest demographic on the road today. According to the Centers for Disease Control and Prevention (CDC), motor vehicle crashes are “the leading cause of death for U.S. teens.”

What’s more, the CDC points out that in 2016, 2,820 teens between the ages of 16 and 19 were killed behind the wheel, and 235,845 were treated in emergency rooms for motor vehicle crash injuries. “That means that six teens ages 16-19 died every day from motor vehicle injuries,” writes the CDC.

Furthermore, the Insurance Institute for Highway Safety (IIHS) says teenagers “drive less than all but the oldest people, but their numbers of crashes and crash deaths are disproportionately high.” In the United States, teens have a crash rate per mile driven that is three times that of drivers 20 and older. The IIHS also points out that in 2013, teens represented only 7 percent of the U.S. population but accounted for 11 percent ($10 billion) of the total costs of motor vehicle injuries.

This data, say industry analysts and experts, is why it’s so expensive to add a teen driver to an existing auto insurance policy, and a recent annual insuranceQuotes survey once again supports this thesis.

How much will a teen driver cost your insurance rates to jump?

According to the insuranceQuotes study, U.S. families who add a young driver to their existing auto insurance policy will see an average annual premium increase of 82 percent (up from 78 percent last year). This might shock some, but according to Mike Barry, vice president of media relations for the nonprofit Insurance Information Institute, it’s an equitable and unavoidable reality.

“Unfortunately, teens just aren’t very good drivers because they don’t have much experience behind the wheel,” Barry says. “Teens are twice as likely to be involved in an accident and 50 percent more likely to be involved in a fatal accident. Anytime you add a driver that is likely to be involved in more accidents as well as more serious accidents, the rise in insurance costs will be steep.”

The good news for parents is that teen driving data is trending in the right direction, even if the needle moves slowly toward increased safety.

For instance, the IIHS reports that there were nearly 10,000 teen driver deaths in 1975, a figure that has continued to drop substantially every year since. And while more than 2,800 teens died in motor vehicle crashes in 2016, that’s 68 percent fewer than the high water mark 40 years prior.

Even recent trends are promising. According to the National Highway Transportation and Safety Administration (NHTSA), fatal crashes amongst drivers between 15 and 20 are down 43 percent from the 7,493 involved in fatal crashes in 2006.

According to Kathy Bernstein, senior manager of the National Safety Council’s Teen Driver Initiative, there are several factors at play here, including the improved safety of modern vehicles, the fact that fewer teens are on the road than ever before, and the continued positive impact of graduated driver’s licensing programs (GDL) across the country.

According to a 2012 study from the University of Michigan, 80 percent of Americans between the ages of 17 and 19 had a driver’s license 30 years ago. Today it’s fewer than 60 percent.

What’s more, a recent IIHS analysis of teen crash deaths shows that fatality rates have plummeted since 1996, the year that states first began enacting GDL systems. The greatest decline occurred among 16-year-olds, with fatal crashes dropping by 68 percent between 1996 and 2010. Fatal crashes fell 59 percent for 17-year-olds, 52 percent for 18-year-olds, and 47 percent for 19-year-olds.

“When you look at the last 15 years or so, as states have implemented these programs, there has been a lot of success in reducing fatal crashes,” says Anne McCartt, the highway safety institute’s senior vice president for research. “But there are still improvements to be made.”

Cost varies depending on age and gender

Not all teen drivers are created equal, and it you’re thinking about adding a teen to your existing policy you should know that the cost will differ depending on the teen’s age and gender.

According to the Insurance Quotes study, it’s more costly to add a young male driver than a female driver to an existing policy. According to Barry, that’s because insurers know young men are statistically riskier drivers than young women.

The study found that adding a male teen to a married couple’s policy results in a national average premium increase of 93 percent (up from 89 percent in 2017).

However, the average increase for adding a female teen is 70 percent (up from 66 percent in 2017).

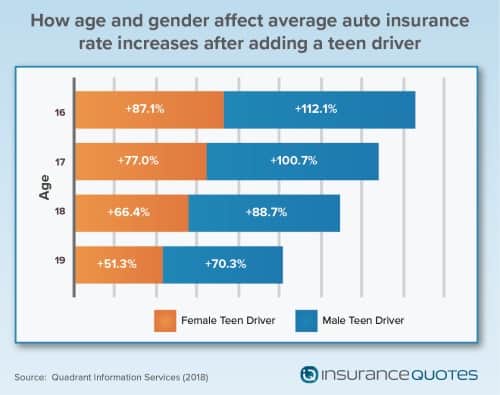

Age also plays a significant role in determining premium increases. For instance, the average premium increase is highest for a 16-year-old male driver (112 percent) and diminishes each year through age 19, when premiums increase by 70 percent, on average.

Meanwhile, the average premium increase for females is also highest at age 16, resulting in an average spike of 87 percent. These figures also diminish as a female teen driver ages, bottoming out at 19 years old with an average annual premium increase of 51 percent.

“Driving well takes practice, and since all teens are new drivers they make all sorts of mistakes that more seasoned drivers can avoid,” says Eli Lehrer, president of the nonprofit R Street Institute. “Also, teens—particularly male teenagers — are inclined towards all sorts of foolish intentional behavior that they eventually outgrow.”

Teen insurance costs vary state by state

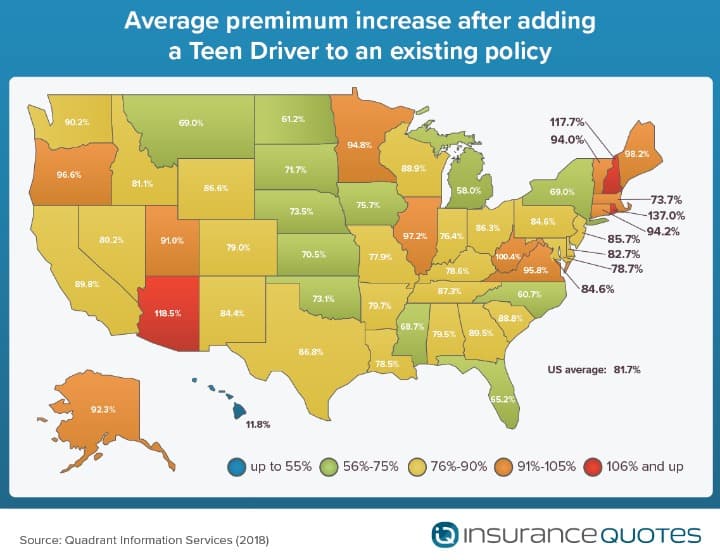

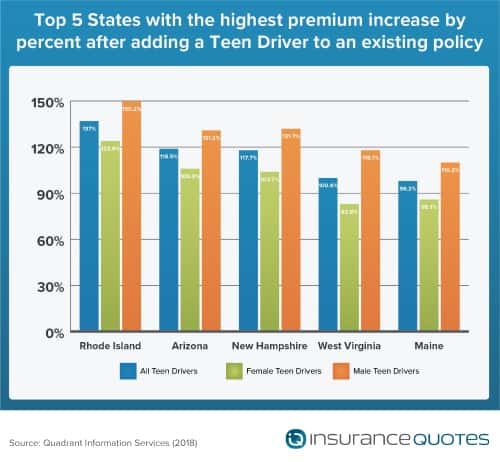

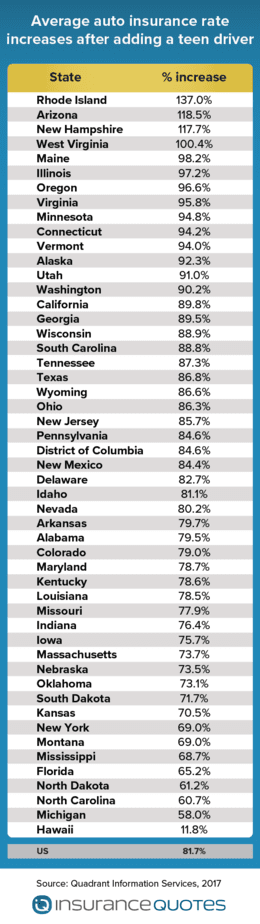

Once again the insuranceQuotes study found that not all states are created equal when it comes to the cost of insuring a teenage driver. For instance, adding a teen to a married adult’s auto policy in Rhode Island will result in an average annual premium increase of 137 percent. In Hawaii, however, the average increase is just 12 percent.

Here are the five most expensive states for car insurance, on average, for adding a teen driver to an existing auto policy:

1) Rhode Island — 137 percent increase

2) Arizona — 118.5 percent increase

3) New Hampshire — 117.7 percent increase

4) West Virginia — 100.4 percent increase

5) Maine — 98.2 percent increase

Meanwhile, here are the five least expensive states, on average, for adding a teen driver to an existing auto policy:

1) Hawaii — 11.8 percent increase

2) Michigan — 58 percent increase

3) North Carolina — 60.7 percent increase

4) North Dakota — 61.2 percent increase

5) Florida — 65.2 percent increase

As always, the reasons behind these differences are somewhat complicated and difficult to pin down, but it starts with the fact that each state regulates insurance differently, and those regulatory differences account for some of the variations in the study’s findings.

For instance, Hawaii (which the National Association of Insurance Commissioners ranks as the 31st most expensive state for auto insurance) is the only state that doesn’t allow insurance providers to consider age, gender or length of driving experience when determining premiums. That means teens really don’t pay much more than adults for auto insurance.

For instance, Hawaii (which the National Association of Insurance Commissioners ranks as the 31st most expensive state for auto insurance) is the only state that doesn’t allow insurance providers to consider age, gender or length of driving experience when determining premiums. That means teens really don’t pay much more than adults for auto insurance.

This may also account for lower increases in states like Michigan and North Carolina, where insurance is regulated more stringently and rating factors are stricter, which means it’s more difficult for individual insurers to raise and lower premiums.

“To a large extent, the differences between states result from differences in regulatory environments,” Lehrer says. “The states with small differences are states known for having very rigorous rate regulation. In those states, drivers who have better claims behavior and better characteristics pay more than they should in order to subsidize teens.”

To that end, Lehrer adds: “Everyone knows that teenagers are bad drivers. If you’re a good driver and live in a state where teenagers aren’t paying a lot more for car insurance, you’re almost certainly paying more than you really should for car insurance.”

Teen driver safety tips

Regardless of the cost incurred by insuring a teen driver, safety remains the primary concern for parents. Here are some expert tips on how to make sure your young driver is as safe as possible behind the wheel:

- Set a good example. “The best way to ensure your teen will be a safe driver is by establishing safe habits and teaching by example,” says Smith. “Avoid speeding and breaking any minor driving laws. By putting your best foot forward, your teen can hopefully mimic your safe habits.”

- Establish firm rules and consistently reiterate them. Ken Hayes, author of Drive Me To Think, says parents should write down a list of driving commitments that their teen must read and sign. “Then, summarize them on a small card that goes inside the car and must be read before each and every time they drive,” says Hayes. “This practice helps focus the mind on their commitments and when those commitments are of a higher nature, they are much more likely to be adhered to.”

- Ask your agent about pay-as-you-drive programs. Otherwise known as usage-based insurance (UBI), pay-as-you-drive programs are now offered by some of the county’s largest insurance providers, including Progressive, Allstate, State Farm, Travelers, the Hartford, Safeco and GMAC. The concept is rather simple. UBI programs are voluntary and drivers can earn discounts based on how well, how far and how often they drive. This is accomplished through the use of telematics devices, which record data regarding driver behavior and then transmit that to insurers to help set the discount.

- Consider electronic monitoring devices. Many insurance companies now offer the installation of devices that monitor driving and flag risky behavior like speeding, aggressive driving, and the non-use of seatbelts. Some devices can even pinpoint a vehicle’s location and let parents dial directly into the car if an alert sounds. What’s more, a recent IIHS study indicates that teens in vehicles with monitoring devices take fewer risks while driving than unsupervised teens.

- Emphasize the dangers of distracted driving. According to NHTSA, research has found that dialing a phone number while driving increases a teens risk of crashing by six times, and that texting while behind the wheel increases that risk by 23 times. Smith suggests not only reiterating these dangers again and again, but also (as always) leading by example. “If you’re texting or talking while driving, they’re going to think it’s okay,” says Smith. “Your mantra should be ‘Do as I say and as a I do.’”

Final Thoughts: Teen Drivers & Car Insurance

The average cost of adding a teen driver to your car insurance can range from $1,800 to $2,300 yearly depending on a few factors and which insurance provider you have. A teenage driver will pay more for auto insurance coverage if they are placed on their own individual policy – up to 300% more. It is a good idea to compare multiple insurance quotes when adding your teen driver to your policy to get the best price.

You can expect your auto insurance costs to raise as much as 82% when adding a teen driver. This will be determined by your insurance companies average rates, the gender and age of your teenager, and what state you live in.

Methodology

insuranceQuotes commissioned Quadrant Information Services to calculate the economic impact of adding a driver between the ages of 16 and 19 to a family’s existing auto insurance policy. Averages are based on a married and employed 45-year-old male and 45-year-old female who each drive 12,000 miles per year and have clean driving records and good credit. Policy limits include $100,000 for injury liability, $300,000 for all injuries, a $500 deductible on collision and comprehensive coverage, and uninsured motorist coverage.

- About the Author

- Latest Posts

Michael Giusti is a senior insurance analyst, business journalist, and university professor with over 20 years of experience. He serves as department chair at Loyola University New Orleans and contributes to Insurance Thought Leadership, U.S. News, and other leading financial outlets.