Why Auto Insurance Claims Get Denied

The concept seems straightforward on the surface: We buy car insurance assuming it will come to our aid after an accident, whether to pay for vehicle repairs or help ease the financial burden of personal injury.

But sometimes things don’t work out in our favor and a claim gets denied, which is not only frustrating and tiresome, but often times expensive.

Even if you’ve done everything right you still may wind up with a denied claim. If that happens, you have some options.

First, every insurance company has an internal appeal process accessible to its policyholders, and if you feel like your claim was treated unfairly you can formally ask for an appeal of the decision.

If that is also denied you should then consider reaching out to your state’s department of insurance to file a complaint while also possibly contacting a lawyer.

For instance, the National Association of Insurance Commissioners provides a thorough list of every state’s insurance department and important contact information here.

At the end of the day you can’t just rely on what your insurance company tells you. You need to do your own research, keep your own records, and seek outside, independent opinions, because this is your life – your car, and your future at stake. If you believe your auto insurance claim should have been approved, learn how to appeal a denied auto insurance claim here.

Common Reasons an Auto Insurance Claim was Denied

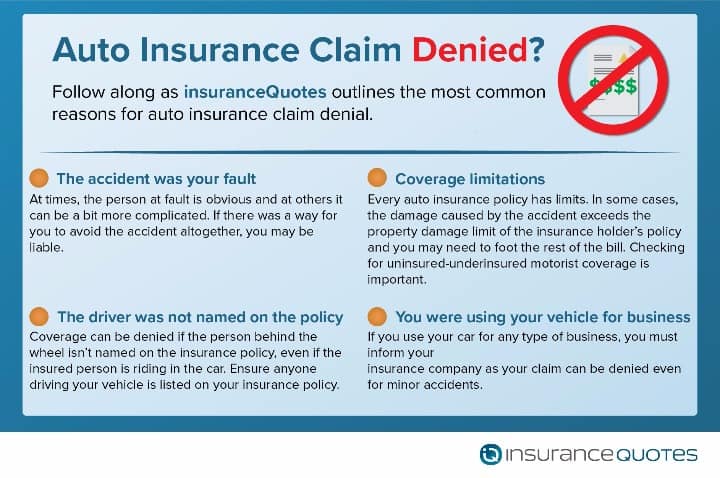

1. The accident was your fault:

Sometimes fault is obvious. For instance, if you cause an accident because you ran a stop sign or were under the influence, your auto insurer is not going to pay up. However, there are more subtle instances where fault is a tricky beast.

For instance, let’s say you’re stopped between two cars at a red light. Suddenly, the car behind you gets rear-ended, causing a chain reaction that ends with you hitting the bumper in front of your vehicle. In the eyes of your insurer, that hit is on you.

“This always infuriates consumers,” Lynch says. “But the fact is you hit the car in front of you. And your insurance company will say that you weren’t responsible for starting the chain of events, but had you been back further you wouldn’t have hit the other driver’s bumper.”

2. Auto insurance coverage limits were met:

Every auto insurance policy provides specific limits on how much will be paid out for various types of claims, and knowing these limitations is critical.

Let’s say, for example, a driver smashes into your $150,000 sports car and totals it. You assume the damages will be covered — until you learn the at-fault driver had a property damage limit of $50,000. In this case, you could find yourself $100,000 in the hole.

“This is why uninsured-underinsured motorist coverage is so important. Too many drivers don’t understand this until it’s too late,” says Amy Bach, executive director of the California-based nonprofit consumer advocacy group United Policyholders. “What’s more, it’s important to understand the coverage limits on your own policy.”

3. The driver was not named on the insurance policy:

Several years ago Linda Schmidt rode as a passenger while her 16-year-old daughter was behind the wheel logging important drive time with her learner’s permit. That afternoon Schmidt’s daughter failed to stop quickly enough and rear-ended another vehicle at an intersection. When they went to file a claim Schmidt’s insurer said the accident wasn’t going to be covered because the Schmidts never informed the insurer that the 16-year-old would be driving the vehicle. “If anyone in your household is going to be driving your vehicle, he or she needs to be named in the policy no matter what,” Lynch says.

4. You were using your vehicle for business:

Let’s say you’re a freelance graphic designer and you often use your vehicle to deliver prints to clients. You need to let your insurer know you sometimes use your car for business purposes. Otherwise, even the most minor accidents might not be covered. “Your insurance company will ask you what you were doing when the accident occurred. And if you say you were delivering prints to a client but the insurer never knew you used your car for business purposes, that claim might be denied,” Lynch says.

How to File an Auto Insurance Claim the Right Way

The aftermath of any accident can be a stressful and intimidating situation. However, it’s critical that you maintain a level head, because how you handle the claim process can make all the difference in whether or not you will be covered.

1. Take photos and document everything:

Immediately following an accident you need to start documenting the situation, and that begins with taking as many photos as possible, including damage to your car, damage to other cars, and the overall accident scene.

“Even if you’re injured, try to get someone else to take photos for you,” Bach says. “It’s always best to gather your own evidence rather than rely on the evidence of others.”

What’s more, make sure you save all documentation related to injuries and damages to your vehicle.

“Many people will try to just say that they suffered a loss, like their bumper was crushed or their neck hurts, but they don’t have documentation to back it up,” says Sally Morin, a San Francisco-based personal injury attorney who focuses on auto accident cases. “You have to submit all records and billing to get paid, which means you need to be very detailed in obtaining and keeping all documentation related to the accident.”

2. Never admit fault:

Sure, the particular circumstances of an accident can be fuzzy and confusing. And sure, you may be a little uncertain about who was to blame. Nonetheless, you should never admit fault.

“It is vital to be clear that the other driver was at fault for the accident and not you,” says Washington, D.C.-based attorney Tom Simeone. “In some states if you are even one percent at fault you are barred from recovering on a claim. It can seriously hurt your case if you say you were — or might have been — at fault. That statement can be used directly against you, even if you later try to amend it.”

3. Never admit to being uninjured:

Adrenaline is a powerful chemical, and it can often mask injuries at the site of an accident we might otherwise feel a few days later.

“A lot of times people will have an accident and walk away feeling fine, but over a period of days, and sometimes even weeks, signs of injury can begin to appear,” says personal injury lawyer Craig Miller, adding that insurance adjusters have “all sorts of tricks” they employ to get you to admit that you weren’t injured.

“They might call up and say, ‘How are ya feeling today?’ You may casually reply that you’re feeling fine, and they may be able to use that as evidence that you weren’t injured in the accident,” Miller says.

Even if you do feel pain, don’t mention it to the adjuster. It may just be what is known as a “masking injury.”

“For example, you may feel pain in your neck, but that’s not the primary injury,” says Atlanta-based personal injury attorney Robert Katz. “It may only be masking pain you will eventually feel in your back a few days later. But if you only mention the neck pain, it could preclude you from compensation for the back pain when it creeps up later on.”

4. Don’t sign anything and don’t consent to being recorded:

Never sign a medical authorization allowing the insurance company to gather your medical records. If you are making an injury claim and you do not hire an attorney, once you are done being treated it’s a smart idea to gather your bills and records yourself.

What’s more, if another driver’s adjuster contacts you and asks to record the conversation you should respectfully decline.

“Drivers are advised to avoid giving recorded statements, which is something that most adjusters demand,” says Jordan Perch, driving expert and blogger for DMV.com. “If the adjuster is allowed to record the conversation, he or she might use the tape later to try and find potential flaws and inconsistencies in the driver’s statement that could hurt the value of his or her claim. Drivers are not required by law to give recorded statements.”

However, Simeone points out that you have a duty to comply with your own insurance company, so if they want to take a recorded statement you need to do it in order to not lose coverage.

5. Don’t let the auto insurance adjuster rush you:

You are entitled to a detailed and thorough claim process, so make sure the adjuster isn’t intimidating you. What’s more, don’t assume that you need to accept the first appraisal that comes in.

“You might want to get things settled as quickly as possible, but there’s probably more money available from the insurance company than the adjuster is offering at first,” Bach says. “The first offer is almost never their best offer, so if you feel like you are capable of negotiating for more, you should.”

6. Don’t assume your insurer is your friend:

Simeone points out that every statement made to an insurance company, including your own, is not protected by attorney-client privilege, which means the adverse insurance company can obtain any statements you gave to your own insurance company with a letter or, if litigation occurs, a subpoena.

What’s more, if the at-fault driver has no insurance or loses coverage for some reason, your own insurance company may have to pay claims on his or her behalf.

“That means your own insurance company can end up being adverse to you in the sense that it wants to pay you as little as possible,” Simone says. “This is another reason not to just blindly confide in your insurance company or trust them to give you advice.”

7. Only answer the question asked:

In addition to standard questions about the nature of the accident, an insurance adjuster will also add more pointed questions that you need to be prepared to answer. For instance: Who, in your opinion, had the last opportunity to avoid the accident?

“The reason they ask this is because even if the other driver hit you, you could still be held partially at fault if you had some sort of opportunity to avoid the accident at the last second,” Lynch says.

If this comes up, Lynch recommends the following reply: “I’m assuming the person who hit me had the last opportunity to avoid the accident.”

No matter what, Lynch says you should always be honest, but don’t volunteer any more information than is necessary, because you don’t know what it will be used for in the future.

“If they ask you what time it is, don’t tell them how to build a clock,” Lynch says.

- About the Author

- Latest Posts

Michael Giusti is a senior insurance analyst, business journalist, and university professor with over 20 years of experience. He serves as department chair at Loyola University New Orleans and contributes to Insurance Thought Leadership, U.S. News, and other leading financial outlets.