Health Care Then and Now

In 2010, the Affordable Care Act (ACA) − also known as Obamacare − was signed into law, requiring all Americans to have health insurance coverage by 2014.

The plan promised to expand health care coverage, offer financial assistance to lower-income individuals and families, require large employers to cover most of their employees and put a stop to insurance companies dropping the coverage of the sick and not offering coverage for pre-existing conditions.

The question is: Has the Affordable Care Act delivered on its promises?

It’s an important question − especially to groups traditionally uninsured or underinsured, such as people experiencing material poverty (and some of the middle class), young people, and minorities − which is why we gathered data from the U.S. Census Bureau and CDC and compared the percentages of those insured before the ACA and those insured today. We wanted to see how Obamacare has changed the health care landscape in the U.S. so far. Continue reading to see what we found.

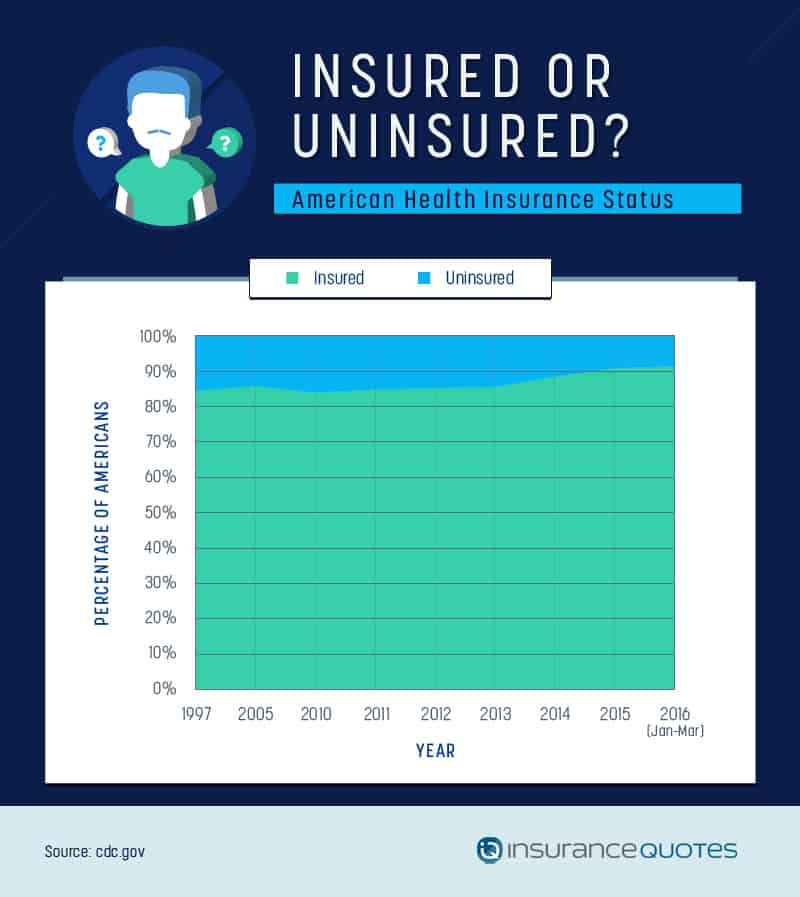

Are More Americans Insured Today?

In 1997, about 15 percent of the population was uninsured, while roughly 23 percent were on public health insurance, according to the CDC. In 2016, those numbers changed − with 36.2 percent reporting public insurance and 8.6 percent uninsured.

The increase in health insurance enrollment was greatest in states that expanded their Medicaid programs, while states that did not adopt the expansion − like Texas and Virginia − still had a large number of residents who were uninsured.

Meanwhile, private insurance has remained relatively steady in its enrollment, hovering between 60 and 70 percent over the last 10 years, with a 63.8 percent enrollment rate in 2016.

Insurance Equity

Financially insecure people were greatly impacted by the ACA. In 2010, nearly 30 percent of those considered financially unstable were uninsured. By 2016, that number had been cut by almost 40 percent.

Not only has the law “pushed back against inequality” by providing coverage to those most in need, but it has also enabled people experiencing material poverty to move toward financial security. According to The Washington Post, “the expansion of Medicaid reduced balances in collections (excluding medical debt) by $51 to $85 on average for all working-age consumers living in those ZIP codes.”

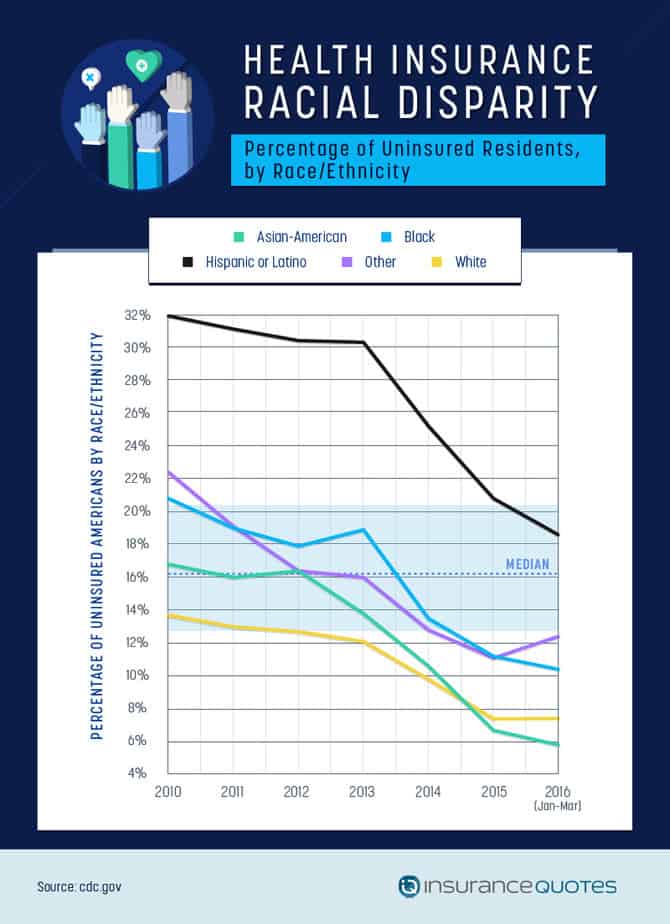

Obamacare and Racial Disparity

Before the Affordable Care Act, the only group with over 85 percent of its members covered by insurance was white people. As recent as 2013, the number of Hispanic individuals uninsured was nearly three times as high as that of white individuals.

The Affordable Care Act has demonstrably lowered this racial disparity in health care coverage, with substantial drops that have taken black, Asian-American, and other populations well below the 15 percent uninsured mark and dropped the uninsured Hispanic population to about 40 percent.

It may be too soon to know the full extent of the impact this increased coverage will have on historically underinsured communities. Per the U.S. Department of Health and Human Services, 8.8 million Latinos covered under private insurance now have access to cervical cancer screenings (a disease with slightly higher incidence rates among the Hispanic population), mammograms, and flu shots with no copay. Additionally, 913,000 Latino young adults (19 to 26 years old) qualify for coverage under their parents’ plans.

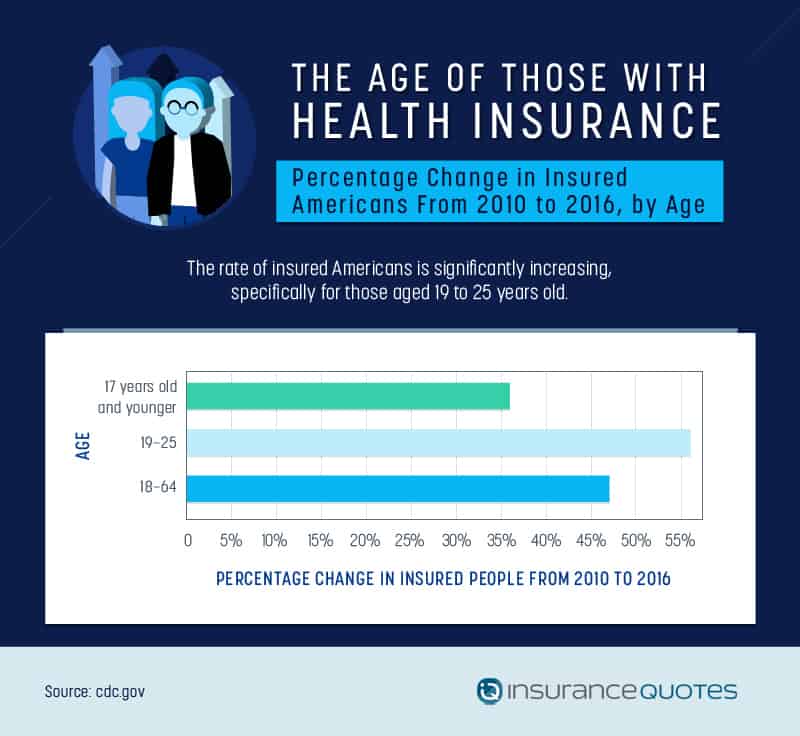

Youth and Obamacare

Another group that has seen substantial increases in health care coverage since the ACA came into effect are Americans aged 19 to 25 years old − a group that has been subject to high unemployment rates. From 2010 to 2016, this group saw an astonishing 56 percent drop in uninsured individuals, with nearly 35 percent reporting no insurance in 2010 to just under 15 percent reporting no insurance in 2016.

However, while enrollment is up for this age group, a notable number of young people remain uncovered, citing affordability as a deciding factor and opting to go without treatment for minor − and even major − issues.

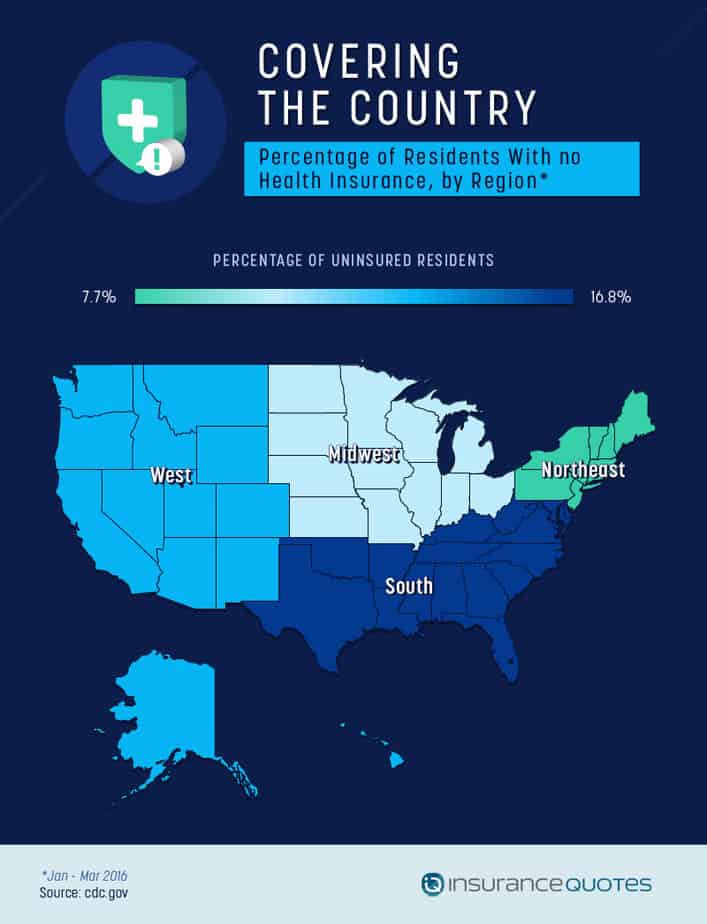

Coverage, by Region

According to the CDC, the region still struggling with a higher-than-average uninsured population is the South − a region that also has the highest number of states that have not adopted the Medicaid expansion.

The states that have chosen not to expand Medicaid are concerned about the eventual cost of the program, while those in favor of the expansion point out that in 2008, the cost of caring for uninsured patients in hospitals was $10.6 billion, so that cost could possibly be reduced by more expansive coverage.

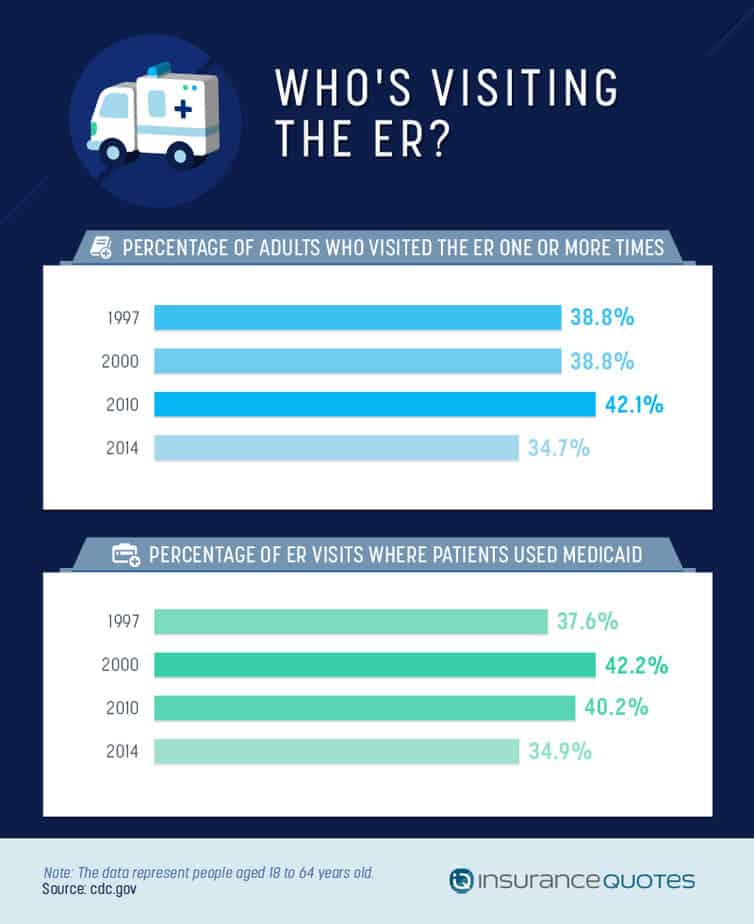

Impact of the ACA on Emergency Rooms

As coverage expands across the U.S., visits to the emergency room are declining − from 38.8 percent of adults visiting at least one time in 1997 to just 34.7 percent in 2014. This drop may be related to previously uninsured people now using primary care doctors to proactively monitor their health rather than the ER.

The percentage of ER visits where patients used Medicaid has also dropped since the Affordable Care Act went into effect. The use of Medicaid − a government program that helps low-income individuals pay for health care − may be on the decline because more low-income people have access to regular health insurance with the help of Obamacare supplements.

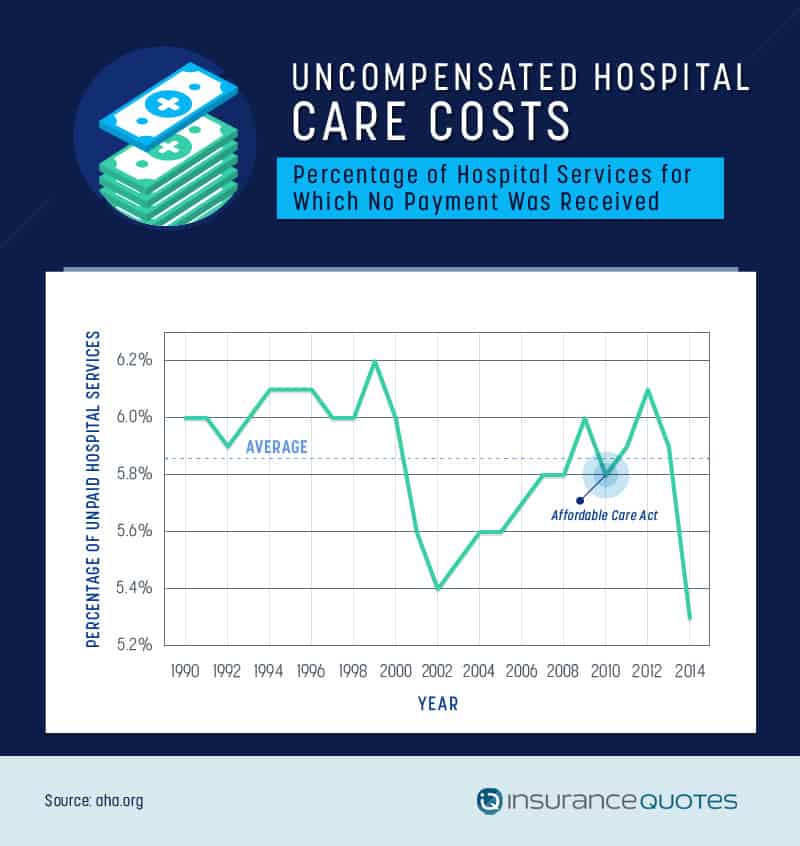

Hospital Costs and the ACA

In the late ’90s, before the Affordable Care Act, the percentage of hospital services for which no payment was received was on the rise, peaking at 6.2 percent in 1999. When the ACA mandated that insurance companies could no longer refuse coverage to people with pre-existing conditions, that number dropped by almost a full percentage point in 2014, with only 5.3 percent of hospital bills going unpaid.

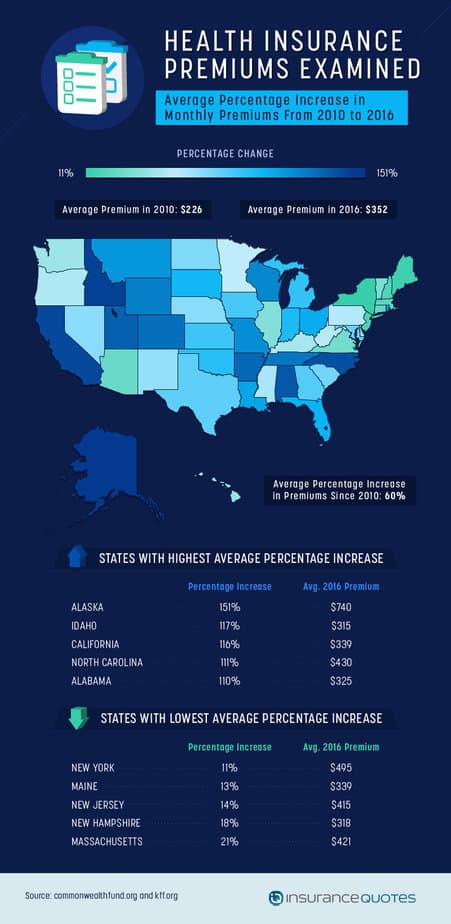

Cost of Premiums: Then and Now

While coverage has increased across the board − and groups that were traditionally uninsured or underinsured are more covered than ever before – not all the news on the Affordable Care Act is good. Since the ACA was signed into law, health insurance costs have risen significantly across the U.S. The average premium in 2010 was $226 per month. In 2016, that number is $352.

Some states have taken a harder hit than others. The increase in Alaska was an astounding 151 percent, while Idaho, California, North Carolina, and Alabama saw increases over 100 percent. The lowest increase in the U.S. was in New York (11 percent) − a number that may still feel significant to those paying the premiums there.

With these premium increases, how is it that the impoverished and young are more covered than ever before? The answer is most likely the cost-assistance programs that turn $400-per-month insurance plans into $100-per-month plans for those whose income qualifies them for federal assistance.

Health Care Today

With health insurance enrollment considerably on the rise (particularly with minorities, young people, and other groups historically less-covered) and hospital losses for uninsured patients decreasing − especially in states that expanded Medicaid − Obamacare seems to be delivering on at least some of its promises.

GOP candidates have called the Affordable Care Act a “job-killer,” but the fact is that unemployment is down and corporate profits are up. Unfortunately, U.S. debt is also up, though how much that is tied to health care is up for debate.

At the end of the day, the ACA is still new, and changes introduced to the U.S. economy are still ongoing, especially as more states consider expanding Medicaid. Time will paint a fuller picture. The good news is that several years into its implementation, the law’s effects include a lessening of the racial, age, and low-income inequality previously widespread in American health care.

SOURCES

http://obamacarefacts.com/howdoes-obamacare-work/

http://www.nytimes.com/interactive/2014/10/29/upshot/obamacare-who-was-helped-most.html?_r=0

https://www.cdc.gov/nchs/data/factsheets/factsheet_disparities.pdf

http://www.hhs.gov/healthcare/facts-and-features/fact-sheets/aca-working-latino-community/index.html

http://www.cdc.gov/cancer/cervical/statistics/race.htm

http://www.bls.gov/web/empsit/cpseea10.htm

http://kff.org/health-reform/slide/current-status-of-the-medicaid-expansion-decision/

http://obamacarefacts.com/obamacares-medicaid-expansion/

http://obamacarefacts.com/2015/05/05/study-shows-er-visits-up-under-aca/

http://obamacarefacts.com/costof-obamacare/

REUSE GUIDELINES

To share this content with your audience make sure it’s done non-commercially, and the URL to link back to this article is present.

- About the Author

- Latest Posts

Lauren Pezzullo is an insurance content strategist and consumer trends analyst. She has led editorial teams at major brands and written for the Center for Health Communication at UT Austin. Her work covers home, auto, and health insurance topics.