Only 8% of Americans Have an HSA and May Be Missing Out on Savings

Health savings accounts (HSAs) provide many financial benefits for consumers. But a new survey shows that many Americans are not taking advantage of them or are confused about how they work.

A new survey from insuranceQuotes.com shows only 8 percent have an HSA, but 50 percent say they’re somewhat or very likely to use one to cut their tax bill. And 31 percent said an HSA would make it easier for them to pay their medical bills.

However, some of those interested consumers might face a problem: lack of knowledge about HSAs. The survey of about 1,000 U.S. adults, conducted in February 2014 by Princeton Survey Research Associates International, shows many Americans don’t know how you qualify for an HSA, which medical expenses you can pay for using the account or what financial benefits you can get.

It’s not surprising many Americans aren’t clear on the ins and outs of HSAs, says Tom Licciardello, a Massachusetts certified financial planner professional and owner of Licciardello Financial Services, who handles health insurance as part of his practice. “It’s a very complex thing to try to explain,” he says.

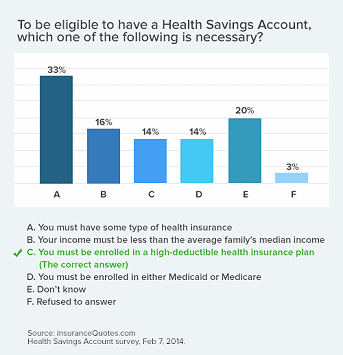

What do consumers know about HSAs?

The survey showed that most Americans don’t understand the basic requirement to qualify for an HSA. Only 14 percent of Americans surveyed knew that you must have a qualifying high-deductible health plan (HDHP) in order to get an HSA. Thirty-three percent mistakenly answered that you simply need some kind of health insurance, while 16 percent mistakenly said your family’s income must be less than the average family’s median income in order to qualify.

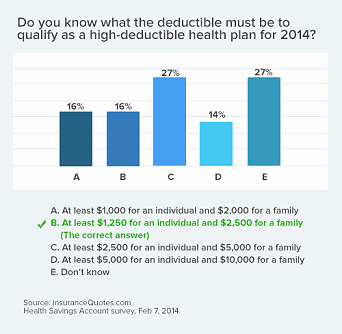

Of the consumers who did know that you must have a qualifying HDHP, most didn’t know how much the deductible must be. For 2020, the minimum deductible for an HDHP is

- $1,400 for an individual.

- $2,800 for a family.

Why choose a high-deductible health plan?

In general, HDHPs have lower premiums than traditional health plans. They provide coverage when you’re hit with big medical expenses only, says Beverly Gossage, a candidate for Kansas Insurance Commissioner and owner of HSA Benefits Consulting.

Consumers shopping on the health insurance marketplaces set up by the Affordable Care Act can choose a high-deductible health plan that qualifies for a health savings account. A qualifying plan must be a HDHP with an individual yearly out-of-pocket maximum of no more than $6,350. Many bronze and silver plans, the most popular plans in the exchanges, meet these standards.

With high-deductible health plans, the insurance company doesn’t pay for any of your health expenses until you reach your deductible, Gossage says. However, there’s an exception. According to IRS rules, an HDHP provide preventive care such as routine exams, cancer screenings and immunizations without a deductible. Under the Affordable Care Act, all health insurance plans inside and outside the exchanges, including employer-sponsored plans, must pay for basic preventive care with no cost sharing before a deductible is met.

One big misconception about HDHPs is that it’s unaffordable for a consumer to pay all medical costs until the deductible is met, Gossage says. But, she says, if you save $100 a month by paying lower premiums, you can put that money into an HSA and you’ll have $1,200 in a year. If you have a large claim, that money can help pay for the deductible, she says. If not, you save money you would’ve spent on premiums for a traditional health plan.

“You buy insurance to cover the big things, not the little things,” Gossage says. “If you really want to make sure the big stuff is covered at the lowest cost possible, you go with an HSA-qualified plan.”

But the survey showed consumers also are confused about how money in an HSA can be spent:

- Fifty-one percent incorrectly stated health insurance premiums can be paid with an HSA. You can only use HSA funds to pay premiums for the following:

- Continuing coverage such as COBRA.

- Coverage while you’re collecting unemployment, Medicare, or other coverage if you’re 65 or older.

- Long-term care insurance.

- Fifty-two percent of Americans stated that HSAs can be used to pay for over-the-counter medication. The only exception is insulin, which can be purchased with HSA funds even without a prescription.

- Twenty-two percent incorrectly believed you can pay for a gym membership with HSA money.

There are a wide range of qualified medical expenses, including acupuncture, ambulance costs, breast pumps, chiropractor fees, doctor fees, dental visits, eyeglasses, fertility services, lab fees, therapy and weight-loss programs to treat a specific disease diagnosed by a doctor, such as obesity or heart disease.

If the IRS determines that you used HSA funds to pay for non-qualified expenses, and you’re under age 65, you’ll be subject to a 20 percent penalty, in addition to ordinary income tax. After age 65, you’ll have to pay taxes only.

What’s the difference between an HSA and an FSA?

Saving money for medical expenses isn’t the only upside of an HSA, Licciardello says.

The money in your account rolls over from year to year, unlike with a flexible spending account (FSAs). An HSA is a medical savings account owned by an individual who has an HDHP. An FSA is an account that does not require an HDHP and allows employees to get reimbursed for qualifying medical expenses. It’s typically funded through withholding from paychecks, and employers also may contribute. An FSA often is described as a use-it-or-lose account because any money not used in a specific time frame reverts to your employer.

However, “an HSA is use-it-or-keep it,” Licciardello says.

You can use the money to pay for medical expenses at any time. Additionally, you may also be able to invest HSA funds and watch the money grow, Gossage says. At age 65, you can start paying your Medicare premiums from your HSA.

“As long as you use that money for qualified medical expenses, you’ll never have to pay tax on that money or on its growth,” Gossage says.

However, you also have another option, Licciardello says. At age 65, you can take withdrawals from an HSA that are subject to ordinary income tax, but not the 20 percent penalty (even if you use the money for something other than qualifying medical expenses.

“It’s another retirement option that is really spectacular,” Licciardello says.

5 Tips for choosing the best HSA

Although some health insurance companies offer an HSA, you have many different options. Use the following tips to find the best HSA for you:

- Watch out for fees. Some accounts charge for monthly account maintenance, debit cards, and certain transactions. Always read the fee schedule and ask questions about any charges that you don’t understand.

- Get the highest interest rate. Some accounts are similar to a regular bank saving that pays a modest interest rate. Others have an investment option where you can choose securities, such as mutual funds or individual stocks.

- Look for no minimum balance. Most HSAs don’t require you to maintain a minimum balance. However, some providers may waive certain fees if you do.

- Make sure you have payment options. Look for accounts that offer both paper checks and a debit card. You’ll be able to pay for medical expenses in just about any situation, either in person or online.

- Get online convenience. Use an account that you can access online for transactions, statements, and records. This allows you to save time and makes electronic payments for your medical expenses.

- About the Author

- Latest Posts

Lauren Pezzullo is an insurance content strategist and consumer trends analyst. She has led editorial teams at major brands and written for the Center for Health Communication at UT Austin. Her work covers home, auto, and health insurance topics.