Study: Bundling Your Insurance Policies Offers Some Surprising Savings

If you’re looking for the easiest way to save money on insurance premiums then bundling your policies is probably the best bet.

Faced with an incredibly competitive market, insurance companies usually offer bundling (or multi-policy) discounts for insuring both your home and car with the same provider. It’s perhaps the most popular way to see significant savings. However, as with all things insurance, the depth of those savings will vary depending on what you’re bundling and where you live.

For the fourth year in a row, insuranceQuotes commissioned a Quadrant Information Services study to examine the average economic impact of bundling auto insurance with either homeowners, condo or renters insurance. Using a hypothetical 45-year-old married woman with a bachelor’s degree, excellent credit score and no lapses in coverage, the study compared the average premium discount for three types of bundling in all 50 states plus Washington, D.C.

The results were once again intriguing to insurance analysts and experts.

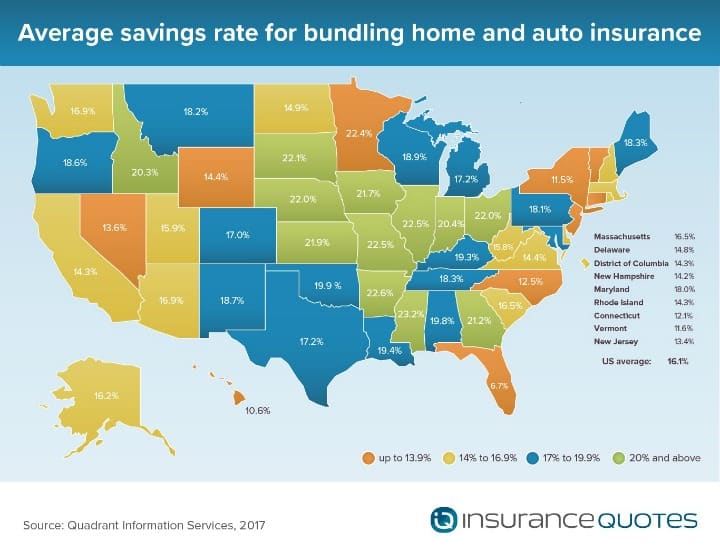

For instance, consumers who bundle auto and homeowners insurance in Mississippi can expect an average annual premium discount of 23.2 percent. However, bundling auto and homeowners insurance in Florida only results in an average premium discount of 6.7 percent.

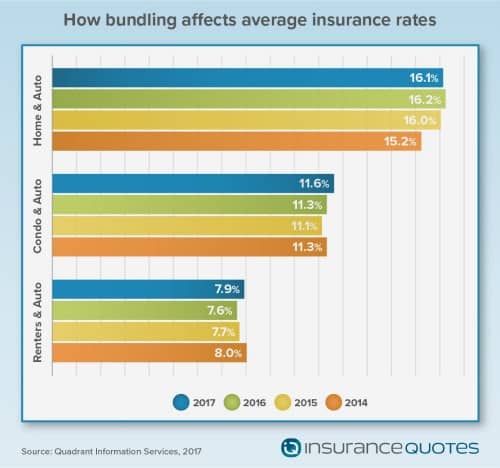

What’s more, bundling discounts will vary depending on what two policies are combined. For instance, the average national premium discount for bundling auto and homeowners insurance is 16.1 percent, but bundling auto with renters insurance will only save consumers an average of 7.9 percent on an annual premium.

Why does bundling save you money?

There’s more than one answer to this question, but at the end of the day bundling discounts stem from two primary factors: retaining loyal customers and saving insurance companies money in the process.

“This all comes down to competition,” says Tennessee-based insurance broker John Hatcher. “There are so many companies out there that can offer lower rates that it’s become harder to keep customers long-term. But the more policies you have with one insurer the longer you are likely going to stay with that company.

“I see this all the time. Everyone wants as many policies on the books as they can get because that means customers will stay with their agency longer.”

What’s more, customers who bundle multiple policies tend to file fewer claims, which winds up saving the insurance company money in the long run, says Arizona-based insurance broker Charlotte Burr.

“Insurance companies, as a whole, find that customers who have more than one line of business with an insurance company tend to be more stable and tend to stick around longer, allowing the insurance company to collect more in premiums — because it’s always cheaper to retain business than find new business,” says Burr, owner of the AZ Insurance Team.

Bundling discounts for home and auto

Once again, bundling auto and homeowners insurance offers the most substantial discount by far. According to the insuranceQuotes study, the national average premium discount for bundling these two products is 16.1 percent.

There are many reasons why this discount is more significant than bundling an auto policy with either condo or renters insurance, says Natasha Rachel Smith, personal finance expert at TopCashBack.com.

“For starters, although insurance companies offer discounts for bundling auto insurance with renters or condo insurance, the savings are significantly smaller,” Smith says.

The main reason is that renters and condo insurance policies are cheaper than homeowners insurance, which means insurance companies can only discount so much.”

The main reason is that renters and condo insurance policies are cheaper than homeowners insurance, which means insurance companies can only discount so much.”

What’s more, insurance companies view homeowners as generally less risky than those who rent or own a condo. That means homeowners are also less likely to file a claim and are therefore allowed deeper discounts.

“Speaking in broad terms, if you look at the stability, financial resources and credit of someone who owns a single family home versus a condo or renter, there are statistical differences between the three,” Burr says. “Usually a home will cost more than a condo, and it’s harder, from a mortgage perspective, to qualify for a home than a condo. So insurance companies figure that if someone has the credit, income and financial history to get approved for a home, they will also probably file fewer claims and maintain their home better.”

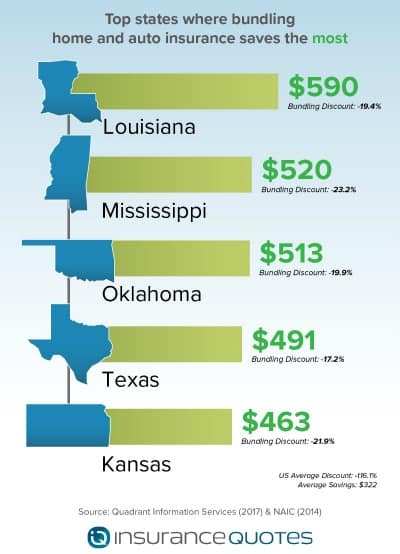

It’s important to note, however, that this discount varies from state to state. Here are the top five states with the greatest average premium discount for bundling auto and homeowners insurance.

- Mississippi — 23.2 percent discount

- Arkansas — 22.6 percent discount

- Missouri — 22.5 percent discount

- Illinois — 22.5 percent discount

- Minnesota — 22.4 percent discount

Meanwhile, the following five states, on average, showed the smallest percentage premium discount for bundling auto and homeowners insurance.

- Florida — 6.7 percent discount.

- Hawaii — 10.6 percent discount

- New York — 11.5 percent discount

- Vermont — 11.6 percent discount.

- Connecticut — 12.1 percent discount

As with all matters pertaining to insurance, these state-by-state differences stem from myriad factors.

For instance, Florida’s unique insurance landscape is a result of continually contending with hurricane and tropical storms threats, which makes both home and auto insurance more expensive and prevents insurers in the Sunshine State from offering substantial multi-policy discounts.

What’s more, every large company that sells homeowners insurance in almost any other state also sells auto insurance. In Florida, however, about 35 percent of the market is written by either the Florida Citizens Property Insurance Corp. — a state entity that doesn’t sell auto insurance — or small state and regional insurers that write homeowners insurance but not auto insurance, which means bundling discounts are often off the table.

“While bundling insurance policies to receive a discount seems like a no-brainer, the types of discounts vary by state and company,” Smith says. “Certain states have a unique set of variables that insurers take into consideration. For example, states that have an elevated risk of hurricanes or natural disasters like Florida tend to pay more to insure their home and automobiles.”

Bundling options for condo and auto

According to the insuranceQuotes study, the national average premium discount for bundling your condo and car insurance is 11.6 percent. The savings are significant, but not as dramatic as homeowners insurance.

One of the reasons for the difference is because insuring a condo is different than insuring a home. If you own a condo you are only responsible for insuring whatever is contained within its walls (not the structure itself). More often than not the condo association is responsible for insuring the building, making condo insurance less expensive than homeowners’ insurance and the discounts less significant.

Nonetheless, discounts still differ between states. The following five states show the greatest average premium discount for bundling auto and condo insurance.

- South Dakota — 16.5 percent discount

- Missouri — 15.8 percent discount

- Illinois — 14.9 percent discount

- Arkansas — 14.6 percent discount

- Kansas — 14.6 percent discount

Meanwhile, the following five states, on average, showed the smallest percentage premium discount for bundling auto and condo insurance.

- North Carolina — 6.7 percent discount

- Connecticut — 7.4 percent discount

- Florida — 7.7 percent discount

- New York — 7.9 percent discount

- New Jersey — 8.4 percent discount

“While not as much as a house, owning a condo does show a certain amount of financial responsibility and an insurance company will take that into consideration by giving some discount, maybe just not as high as a homeowners discount,” Burr says.

Bundling discounts for auto and renters

Even less expensive than homeowners and condo insurance, renters insurance typically covers nothing more than personal possessions, liability, and, in some cases, additional living expenses if a tenant has to relocate. And because it is the cheapest of the three, the discounts offered for bundling are fairly low.

Even less expensive than homeowners and condo insurance, renters insurance typically covers nothing more than personal possessions, liability, and, in some cases, additional living expenses if a tenant has to relocate. And because it is the cheapest of the three, the discounts offered for bundling are fairly low.

According to the study, the national average premium discount for bundling auto and renters insurance is just 7.9 percent.

The following five states show the greatest average premium discount for bundling auto and renters insurance.

- Minnesota — 13.6 percent discount

- Kansas — 12.6 percent discount

- Massachusetts — 11.4 percent discount

- Indiana — 11.4 percent discount

- Missouri — 11.0 percent discount

Meanwhile, the following five states, on average, showed the smallest percentage premium discount for bundling auto and renters insurance.

- North Carolina — 4.5 percent discount

- New Jersey — 4.9 percent discount

- New York — 5.0 percent discount

- Vermont — 5.9 percent discount

- Connecticut — 6.2 percent discount

Whether you own a home, a condo, or rent your place, bundling discounts are one of the easiest ways to not only save money but to also simplify your overall insurance landscape.

“The obvious benefit to bundling your insurance policies is the money you can save, but another benefit is that bundling policies simplifies policy management,” says Jayson Greene, insurance expert with Carolina Insurance Professionals.

“Save yourself the hassle of keeping up with multiple statements and renewal dates by combining your policies under a single insurance provider. Bundling policies makes maintaining statements and policy renewals a breeze. It’s a good deal all around.”

Methodology

insuranceQuotes and Quadrant Information Services calculated the average economic impact of purchasing auto insurance with either home, condo or renters insurance using data from the largest carriers (representing 60-70 percent of market share) in each U.S. state and the District of Columbia. Averages are based on a 45-year-old married, employed female with a clean driving record. The hypothetical driver has a bachelor’s degree, an excellent credit score, no lapses in coverage and the following limits: $100,000/$300,000 (bodily injury), $100,000 (property damage), $100,000/$300,000 (UI/UIM), $10,000 (PIP) and a $500 deductible.

Home: based on single family, 2-story, 1800 square foot, frame home, built in 1976 and the following limits: $140,000 (dwelling), $70,000 (personal property), $300,000 (liability), $5,000 (medical), and a $500 deductible.

Condo: based on $50,000 (personal property), $100,000 (liability), $5,000 (medical), and a $500 deductible.

Renters: based on $50,000 (personal property), $100,000 (liability), $5,000 (medical), and a $500 deductible.

- About the Author

- Latest Posts

Brian O’Connell is a nationally recognized financial journalist, best-selling author, and former Wall Street bond trader with over 20 years of experience. He is the author of The 401(k) Millionaire and CNBC’s Creating Wealth, and has contributed to The Wall Street Journal, U.S. News & World Report, Forbes, CBS News, and TheStreet.