One Home Insurance Claim May Raise Your Premium by Up to 21%

It probably comes as no surprise that filing an auto insurance claim will likely result in a raised annual premium. What may be shocking to some, however, is that filing a claim on your home insurance policy could also result in a hefty rate increase.

A recent study, commissioned by insuranceQuotes.com, examined the average economic impact of filing a single claim on your homeowner’s insurance policy. Using a hypothetical two-story, single family home covered for $144,000 with a $500 deductible, the study revealed how much annual premiums can go up for claims including fire, hail, liability, medical, theft, vandalism, water (non-weather related), weather (except for hail and wind) and wind.

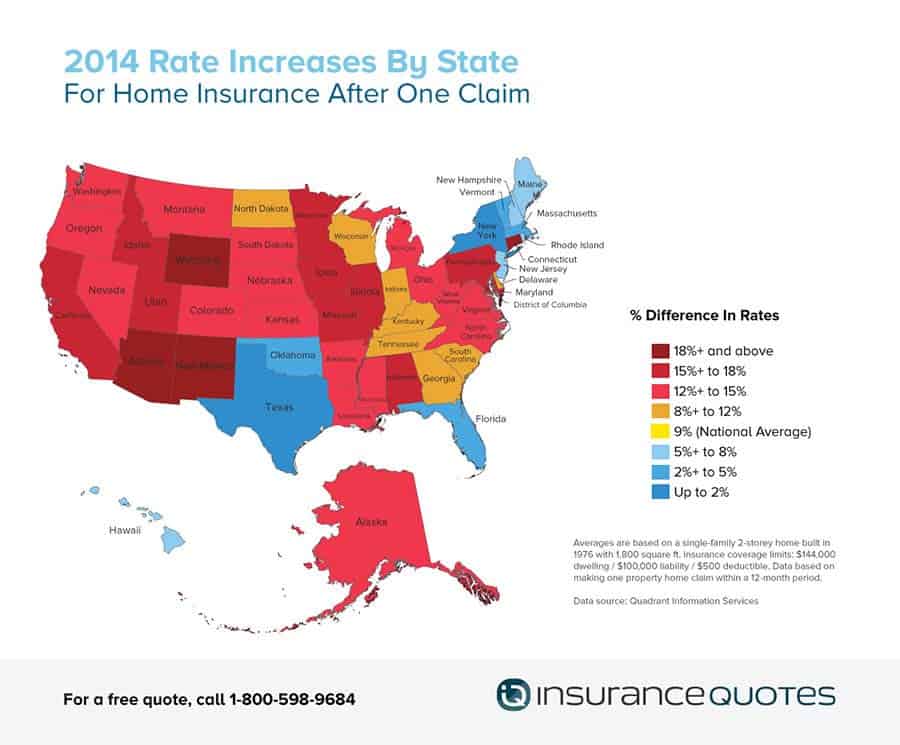

The study compared the average premium increases for all 50 states, and the results were as perplexing as they were intriguing to insurance analysts and experts.

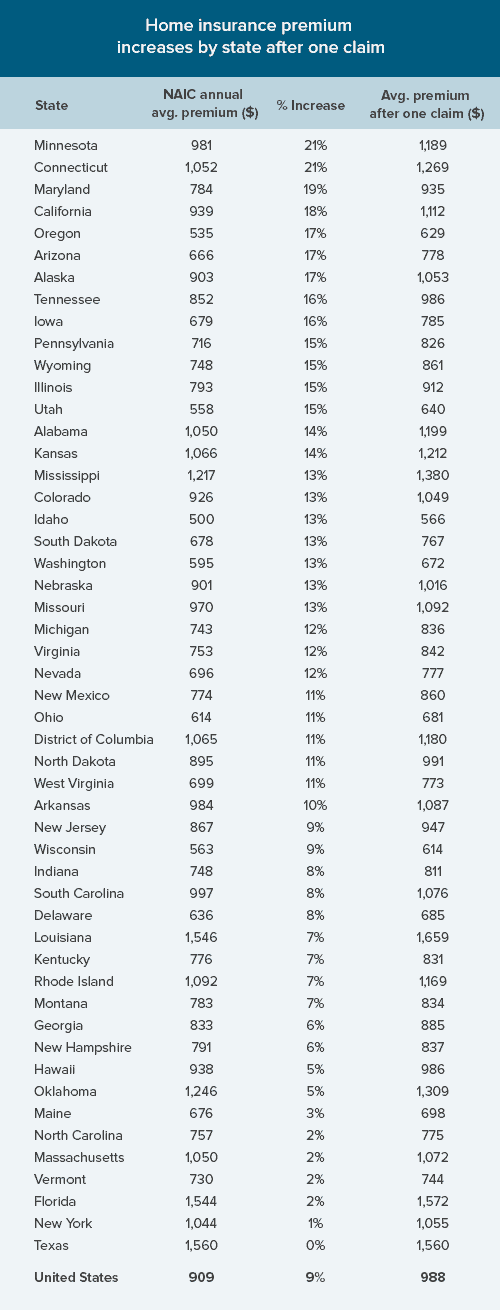

For instance, homeowners who file a single claim in Minnesota can expect their annual premium to increase, on average, by 21 percent. Conversely, filing a single claim in Texas won’t result in any premium increase.

For instance, homeowners who file a single claim in Minnesota can expect their annual premium to increase, on average, by 21 percent. Conversely, filing a single claim in Texas won’t result in any premium increase.

The study’s findings come at a time when most U.S. families are already experiencing an increase in their homeowner’s insurance premiums across the board. According to the latest data from the National Association of Insurance Commissioners (NAIC), the average cost of home insurance increased 36 percent between 2003 and 2010, which is almost twice the rate of inflation.

If you file a home insurance claim, how much will your premium go up?

According to the study, U.S. families who file a singlehomeowner’s insurance claim can expect their annual premium to increase 9 percent (or about $150). However, there are several states that buck the national average.

The following five states showed the greatest average premium increase as a result of filing one claim:

1. Minnesota — 21 percent increase

2. Connecticut — 21 percent increase

3. Maryland — 19 percent increase

4. California — 18 percent increase

5. Oregon — 17 percent increase

Meanwhile, the following five states, on average, showed the smallest percentage premium increase as a result of filing one claim:

1. Texas — 0 percent increase

2. New York — 1 percent increase

3. Florida — 2 percent increase

4. Vermont — 2 percent increase

5. Massachusetts — 2 percent increase

“For homeowners in states where premiums are going up by more than 10 percent for a single claim, that’s a bit troubling,” says Bob Hunter, former Texas Insurance Commissioner and current director of insurance at the D.C.-based Consumer Federation of America, a consumer advocacy organization.

According to the study, premiums in 31 states and the District of Columbia increased by an average of 10 percent or more after filing a single claim. What’s more, only 18 states fell below the national average increase of 9 percent.

See also: When should you file a home insurance claim?

The reasons behind why there is such a disparity from state to state are varied and nuanced, says Chris Hackett, director of personal lines policy at the Property Casualty Insurers Association of America, an insurance trade association. According to Hackett, rate swings between states come from several factors, including the nature and severity of claims filed in a given state, as well as the different ways in which insurance is regulated from state to state.

“You have to keep in mind that insurance is regulated on a state-by-state basis, so that’s going to play a role,” Hackett says. “And different states are faced with different types of risks and claims, which will also affect premium costs. So it’s important to be very careful about generalizing here.”

How state regulation affects insurance rates

According to Amy Bach, executive director of the California-based nonprofit consumer advocacy group United Policyholders, the first thing to consider is how each state regulates its insurance industry and the extent to which individual insurance companies are allowed to increase premiums based on filed claims.

“My assumption is that the states with the smallest increases probably have restrictions on what an insurance company can do to your premium after filing a single claim,” Bach says. She adds, “It’s really not fair to consumers that filing one claim would affect their rates.”

Bach’s theory seems to pan out in the study’s most obvious outlier, Texas, where filing a single home insurance claim won’t change your annual premium at all. According to David Nardecchia, manager of the commercial property and casualty division at the Texas Department of Insurance, Texas insurance law prohibits insurers from increasing premiums on homeowners for filing first-time claims.

According to Hunter, the states that show an average premium increase of less than 5 percent (New York, Florida, Vermont, Massachusetts, North Carolina and Maine) probably have similar premium hike restrictions on the books.

“What I think you’re seeing in those states below five percent is probably a company here and there that tacks on an additional fee after a claim is filed, that’s all,” Hunter says.

However, Eli Lehrer, president of the nonprofit research group The R Street Institute, disagrees.

“I find it most interesting that there seems to be very little correlation between a state’s regulatory regime and the degree to which premiums are impacted,” Lehrer says.

For example, Lehrer points to Illinois, which is widely regarded as the most liberally regulated state in the country (since insurers are free to set rates however they please and are not overseen by the state’s insurance department). There, a single homeowner’s claim will result in an average premium increase of 15 percent.

Meanwhile, California, which is one of the most tightly regulated states in the country (for instance, banning credit scores as a rating factor), shows an average premium increase of 18 percent, the fourth largest on the list.

“I was shocked to find (California) was so high on the list,” Hunter says.

How claim type affects home insurance rates

Since he couldn’t find a correlation between a state’s insurance laws and the average increase to homeowner premiums, Lehrer suggests the numbers may be the result of something entirely different: “The nature of claims from state to state.”

When it comes to insuring homes, Lehrer says, each state has different risks to consider. For instance, an insurance company writing a home insurance policy in Oklahoma will likely consider the prevalence of tornadoes as a risk factor. Meanwhile, an insurance company in Florida is probably going to be more concerned about disasters like hurricanes (but not floods, since flooding isn’t covered by a typical home insurance policy).

This difference between the types and severity of insurance claims—and how accurately companies are insuring against these risks—may play a role in the differences between premium increases from state to state.

Consider, for instance, Minnesota, the state with the highest premium increase (21 percent) after a claim. According to Mark Kulda, spokesman for the Insurance Federation of Minnesota, the average home insurance premium for his state in 1998 was just $368 a year, far below the national average. By 2010 that figure jumped to an average of $961 per year, which is well above the national average.

“That’s a 250-plus percent increase in premium costs, and we can thank natural disasters for that,” Kulda says.

Since 1998, Minnesota has experienced an unprecedented uptick in natural disasters. For instance, in 1998, Minnesota’s insurers experienced $1.5 billion in storm losses—more than the previous 40 years combined. And in 2010, Minnesota suffered from 144 tornadoes, more than three times its annual average.

“Before 1998 we were considered a pretty stable and relatively cheap state to buy homeowner’s insurance,” Kulda says.

Insurance companies in Minnesota need to catch up to a whole new level of claims costs when it comes to insuring people’s homes. One way to do that? Increase premiums more dramatically whenever a homeowner file a claim.

“These numbers may be surprising to some, but it certainly fits within our narrative since 1998,” Kulda says.

Robert Hartwig, economist and president of the nonprofit Insurance Information Institute, points out that Minnesota insurers just haven’t been used to the intense frequency of catastrophic events befalling The North Star State in recent years

Meanwhile, a state like Texas has been insuring against natural disasters for decades, which would explain why they don’t need to raise premiums whenever someone files a single claim.

“Texas is arguably one of the most disaster-prone states in the U.S., so home insurers there set their rates with some expectation of potentially large catastrophic losses already built into the premium,” Hartwig says.

What’s more, Kulda says, Minnesota insurance law bars insurance companies from canceling a policy after one weather-related claim.

“So the only tool insurers have is pricing,” Kulda says. “Insurers may not be able to non-renew your policy or cancel it for a single claim, but they can make your premium go up. The sad part is, even as premiums rise, insurers are still probably not quite caught up yet.”

How to save money on your homeowner’s insurance

No matter where you live, here are three tips to help you save money on homeowner’s insurance.

1. Increase your deductible.

According to Kulda, the first thing homeowners should do is consider whether their deductible is too low.

“It’s pretty rare these days to see a $500 deductible,” Kulda says. “Perhaps you should think about making it $1,000. The higher your deductible the lower your premium is going to be.”

2. Ask your agent about discounts.

According to Hackett, there are myriad discounts available to homeowners, many of which go unclaimed.

“Make sure you’re not overlooking any (discounts) that you might be qualified for,” Hackett says. “For example, if you set up automatic payment through your checking account online, or if you package your homeowner’s policy with your life and auto policies, you could save money over time.”

Hackett adds that many insurance companies are also starting to provide discounts in the neighborhood of 15 to 20 percent if a home is equipped with a security system.

3. Maintain your home.

According to Pete Moraga, spokesman for the Insurance Information Network of California, most homeowners don’t take the time to properly maintain their property.

“We encourage homeowners to take 10 minutes every few months and check the home’s water system,” Moraga says. “Make sure the pressure is good, that nothing is dripping under the sink, and this can save you a lot of heartache and problems in the future. And then also take a look around your house to make sure there are no other potential issues, like a bad roof or dead tree that might result in having to file a claim down the road.”

- About the Author

- Latest Posts

Autumn Cafiero Giusti is a licensed life and health insurance broker and award-winning journalist with more than 20 years of experience. She writes extensively about flood, Medicare, home, and life insurance for publications like U.S. News and CBS News.