Survey: Myths About Insurance Keep Americans Guessing About Coverage

Insurance is an industry of numbers and hard facts that are often mixed with wide-ranging emotions as people often file claims after a devastating life event.

But it also is an industry filled with relentless myths, that, for one reason or another, just won’t go away. For instance, does having a red car really increase your auto premium? Is flood damage covered by a standard home policy? Do women actually pay higher health premiums than men?

The answers to these questions are no, no and yes — respectively — but according to the latest survey commissioned by insuranceQuotes, millions of Americans think otherwise.

RELATED: How to Fight a Denied Insurance Claim

Testing consumer knowledge on home, health, life, and auto insurance, the nationwide 2019 Insurance Myths and Misconceptions survey exposed a lack of awareness on an assortment of insurance-related topics, from what is covered by comprehensive auto coverage to health insurance costs for men versus women, to what life insurance providers are allowed to factor it when determining someone’s premium.

“I think these myths come from a combination of so many people having insurance but also not really understanding how it works,” says California-based insurance agent Tracy Pagliuso. “And that’s not a very good position for consumers to be in. These common myths stick around because most people purchase insurance and then forget about it—until they need it of course.”

In short, being misinformed on insurance can be quite costly—and potentially dangerous—so let’s dive into the truth behind the fiction.

Auto Insurance

According to the Pew Research Center, 88 percent of Americans owned a car in 2018. Given the ubiquity of car ownership one would assume that very few misconceptions about auto insurance would persist, and yet our survey turned up some fascinating and perplexing misapprehensions amongst the driving public.

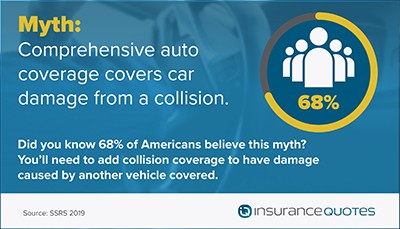

For instance, 68 percent of Americans incorrectly believe that comprehensive auto insurance covers car damage from a collision. This is decidedly not the case.

“I’m always surprised by how confused people get about comprehensive versus collision versus liability coverage,” Pagliuso says. “But at the same time I understand it to some extent. It’s not like this is something you learn in school.”

Simply put, comprehensive auto coverage pays for damage that results from something other than a collision, such as fire, theft or vandalism. Meanwhile, liability insurance pays for the policyholder’s legal responsibility to others for bodily injury or property damage, while collision insurance covers property damage to the policyholder’s car.

According to the National Association of Insurance Commissioners (NAIC), the average cost of a comprehensive claim was $1,817 in 2017 (the most recent data available) whereas the average cost of a collision claim was $3,425.

“If you understand nothing else about how auto insurance works you need to at least understand the difference between liability, comprehensive, and collision coverage,” Pagliuso says. “If you don’t, you might be driving around without the proper type of policy to cover you in the event of an accident, and that can be financially disastrous for some.”

Perhaps slightly less serious — but no less enduring — is the myth that driving a red car means you will pay more for auto insurance. According to our survey, 36 percent of Americans incorrectly believe that having a red car increases auto insurance rates. What’s more, respondents between the ages of 18 and 34 were most susceptible to this myth, with 41 percent of that demographic saying red cars are more expensive to insure.

According to a 2015 statement from Geico, “A red car won’t cost you more than a green, yellow, black, or blue car. Insurers are interested in the year, make, model, body type, engine size and age of your vehicle. How you’re perceived based on the color of your car is another matter.”

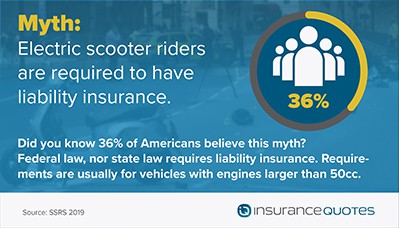

Finally, with the increasing popularity of electric scooters and scooter sharing companies cropping up in U.S. cities, it seems a new myth has emerged, as 36 percent of Americans incorrectly believe that electric scooter riders are required by federal law to have liability insurance.

According to the NAIC, companies such as Lime, Bird, and Spin have rolled out scooter rentals in major cities throughout the U.S. These battery-powered scooters reach speeds of 15 to 20 mph and may or may not require proof of a valid driver’s license. “There are hundreds of scooters in some cities, and they have caused some headaches and have insurance implications for consumers, municipalities, and insurance companies,” writes the NAIC.

And while there have been numerous reports of accidents involving electric scooters over the past few years, there is no federal law requiring riders to carry liability insurance. According to the NAIC, some cities, like San Francisco, “require scooter rental companies to obtain a permit from the city and provide proof of insurance before they can operate legally.”

But unless the scooter rental company — or your local municipality — requires it, liability insurance is not a legal necessity.

Nonetheless, Pagliuso offers a word of caution.

“Even though you aren’t legally required to carry liability insurance, you should at least consider ways to cover yourself,” Pagliuso says. “After all, if you’re interacting with traffic on an electric scooter, you may run into some financial headaches if you’re in an accident.”

According to the NAIC, scooter riders should rely on their health insurance for any medical injury they sustain. Additionally, they encourage scooter riders to check with their auto insurance carriers to determine whether or not they’re covered.

Homeowners Policies

When it comes to insuring a home, the stakes are understandably high. Not only is it probably your most substantial investment, but it also contains your most valuable possessions, some of which may be truly priceless. And this is why it’s critical to understand what is and isn’t covered by a standard policy.

At the top of the misconception list are flood and mold damage. According to the insuranceQuotes.com survey, 35 percent of Americans incorrectly believe that a standard homeowner’s insurance policy covers flood damage. In addition, 34 percent incorrectly believe that a standard homeowner’s insurance policy covers mold damage. These two fallacies can have disastrous consequences.

Let’s first take a look at flood insurance.

Since it is sold and regulated by the federal government, flood insurance is a unique and sometimes complicated segment of the insurance market, and according to Louis Chiafullo, a partner in the insurance practice at McCarter & English, one of the most common misconceptions about flood insurance is that it is included in the average homeowners policy.

“Many homeowners think it’s a basic part of their coverage,” Chiafullo says. “It’s not.”

Flood insurance is an added premium offered by the National Flood Insurance Program (NFIP), a product of the federal government administrated by the Federal Emergency Management Agency (FEMA). In the event of water damage from flooding, the insured homeowner will have coverage up to statutorily set limits for his or her property.

According to the NFIP, a homeowner flood insurance policy covers up to $250,000 in structural damage and up to $100,000 in content loss. A businesses policy covers up to $500,000 in both structural damage and content loss.

But when talking about flood insurance coverage, it’s first important to understand what the word “flood” actually means. Mark Carrasquillo, an agent with the New York City-based brokerage E.G. Bowman Company, says that many homeowners don’t have a proper understanding of the terminology, and therefore don’t understand the precise nature of their coverage.

“Many consumers, when discussing or describing a loss, think that the words ‘flood’ and ‘water damage’ are interchangeable and mean the same thing,” says Carrasquillo. “This is entirely wrong. In the insurance world the terms are very different.”

Flood is defined by the NFIP, in part, as: “A general and temporary condition of partial or complete inundation of two or more acres of normally dry land area or of two or more properties (at least one of which is your property) from overflow of inland or tidal waters, from unusual and rapid accumulation or runoff of surface waters from any source, or from mudflow.”

Water damage, essentially, is everything else. This includes the breaking or cracking of any part of an appliance or system that contains water (i.e. water heaters, baseboards or steam heat, shower pans, toilets, etc.), water backup of sewers and drains, and rising water that may damage a basement. These are not covered by a flood insurance policy.

Another critical caveat in the world of flood insurance concerns the basement. According to Frank Darras, a national consumer litigation lawyer specializing in insurance, the only items covered in your basement are structural elements and essential equipment, which include electrical and HVAC systems.

“Beware — if you have a finished basement with things like a pool table, carpeting, a flat screen TV, or expensive woodwork, they are not going to be covered by flood insurance,” says Darras, adding that fewer than 20 percent of homeowners in the United States currently have flood insurance. “And that,” he says, “is a woefully low number.”

A large portion of that 20 percent comes from homeowners who are required to purchase flood insurance in order to obtain a mortgage. Under the Flood Disaster Protection Act of 1973 and the National Flood Insurance Reform Act of 1994, lenders are mandated to require the purchase of flood insurance by property owners who obtain mortgage loans from federally regulated, supervised, or insured financial institutions for structures located within—or to be located within—a Special Flood Hazard Area (SFHA).

Even if your home is not located in a SFHA, Janet Scott-Buckley, manager of Harrington Insurance Agency’s North Andover, Massachusetts office, says you should still consider purchasing flood insurance.

“The number one misconception is that some people are in a ‘flood zone’ and some are ‘not.’ Everyone is in a flood zone,” says Scott-Buckley. “Even lower risk areas can experience a flood.”

Consider that, according to Darras, about 25 percent of flood insurance claims each year come into the NFIP from properties outside a high flood risk zone. In order to determine the flood zone risk for a particular region, current and prospective homeowners can visit the NFIP’s website at www.floodmsart.gov for access to national flood-hazard maps that detail various levels of risk.

Franklin Reid, vice president for MetLife Auto & Home, says homeowners should frequently check these maps for updates and changes, since new residential development can affect a region’s risk for flooding.

“So much development goes on that actually changes the terrain,” says Reid. “During a torrential rain storm, the flow of the water is now different and can result in some heavy flood activity. We are seeing flood activity in areas of the country that haven’t seen flooding in many years.”

And then there’s mold.

According to the Centers for Disease Control and Prevention (CDC), mold is everywhere—it grows year-round (not just in the summertime) and can be found both indoors and outdoors. It’s a living organism and, as such, it grows and spreads when it has the right conditions.

“I think people have a generally icky feeling about mold but they don’t take it seriously enough,” says Anthony Barton, a longtime Florida-based insurance adjuster who specializes in home insurance claims that frequently involve mold. “Both from a health standpoint and an insurance standpoint, mold needs to be on more people’s radar.”

Barton’s takeaway: Don’t be afraid of the mold and don’t ignore it if you suspect it might be lurking in your home. Find it, remove it, and make sure you know what type of mold damage is and isn’t covered by your homeowners’ policy.

“The bad news is that mold — like rot and insect infestation — s a home maintenance issue, and these are generally not covered by standard homeowners insurance policies,” says Barton.

However, according to the nonprofit Insurance Information Institute (III), “in the event that mold growth is the direct result of a covered peril such as a burst pipe, the cost of eliminating the mold may be covered.” What’s more, if you have federal flood insurance, it may cover you for mold and mildew damage, “but only if it is directly attributable to a flood.”

“I encounter this all the time,” says Barton. “People don’t think they have to worry about mold prevention because they assume that if they find some the remediation will be covered by insurance. But nine times out of ten, it’s not.”

Health Coverage and Life Insurance

Both health and life insurance can be intimidating subsets of the insurance landscape, which may account for why the insuranceQuotes.com survey found two major misconceptions.

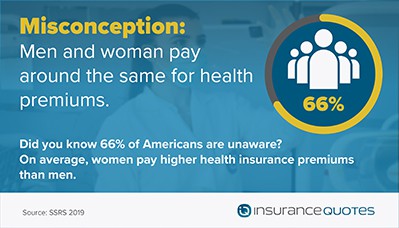

First, according to the survey, 66 percent of Americans are unaware that women, on average, pay higher health insurance premiums than men. To be sure, this disparity has been drastically reduced since the passage of the Affordable Care Act (ACA), which barred the use of “gender rating,” a common practice that often found women paying up to 50 percent more for monthly premiums than men. Now, under the provisions of the ACA, insurance companies are prohibited from charging women more than men.

Nonetheless, a small premium disparity remains. According to data from the analytic website eHealth, men paid, on average, $43 less than women per month for insurance purchased through the healthcare marketplace last year (the average monthly premium for a single woman in 2018 was $461 versus $418 for a single male).

“This is still a controversial topic, as there are some who feel that women should pay more for health insurance because they are statistically more expensive to insure,” says health insurance expert and advocate Janet Fields. “They often use the analogy that young males pay more for car insurance than females, so why not charge women more for health insurance than men. But caring for our bodies is much, much different than caring for an automobile.”

ALSO: How to Select the Best Life Insurance Policy

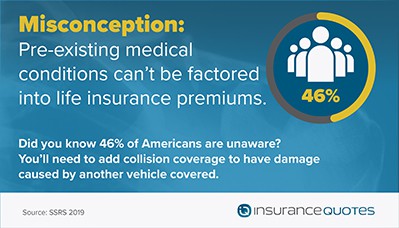

Meanwhile, on the topic of life insurance, the survey revealed that 46 percent of Americans are unaware that life insurance providers are allowed to factor in someone’s pre-existing medical conditions when determining their premium.

The truth is that, from a life insurer’s standpoint, the more health problems you have and the more serious they are, the more at risk you are of dying at an earlier age. This is what will most likely lead to higher premiums. And it’s not just major diseases such as diabetes that can cause premiums to skyrocket. You may also be quoted a higher premium for conditions you can control such as obesity, high cholesterol, and high blood pressure.

The bottom line: If you’re planning to apply for life insurance in the future, be proactive about your health. And if you have a severe preexisting condition over which you have little-to-no control, make sure you shop around for a policy that may be more financially forgiving of the condition.

At the end of the day, some of these myths are more consequential than others. But the solution for consumers remains the same across the broad, regardless of insurance type: conduct research, shop around different providers for the best plan and, most importantly, read the fine print. In life, unexpected circumstances inevitably arise, and having a full understanding of what is covered — as well as what isn’t covered — will help protect your wallet, safety, and peace of mind in the long run.

- About the Author

- Latest Posts

Autumn Cafiero Giusti is a licensed life and health insurance broker and award-winning journalist with more than 20 years of experience. She writes extensively about flood, Medicare, home, and life insurance for publications like U.S. News and CBS News.