Lapse in coverage drives up auto insurance rates — as much as 35%

Plenty of factors can lead to an increase in your car insurance premium, including at-fault accidents and moving violations. But a new study finds that one of the costliest things that can happen to your policy is a lapse in coverage.

A recent Quadrant Information Services study, commissioned by insuranceQuotes.com, examined the average economic impact of a lapse in auto insurance coverage. The study compared the average six-month premium increase for a lapse in coverage in all 50 states plus Washington, D.C., and the results were as intriguing as they were varied.

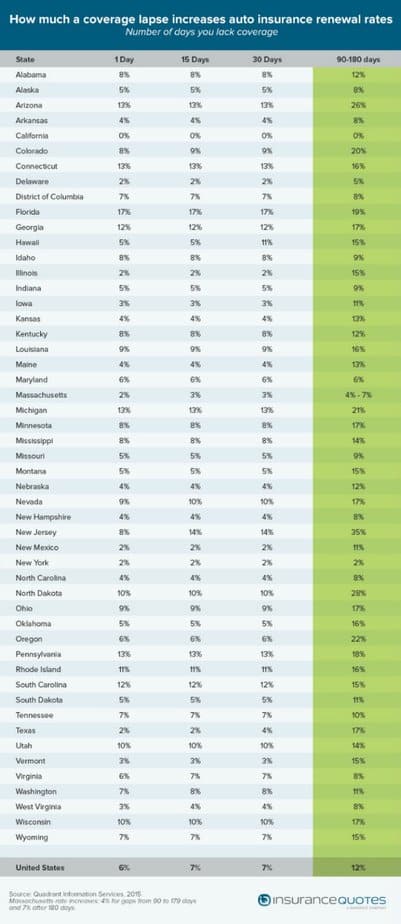

For instance, letting your car insurance coverage lapse for longer than 45 days causes a national average premium increase of 12 percent once the policy is reinstated. What’s more, certain states carry even heavier surcharge penalties after a lapse.

Florida drivers who let their auto policy lapse for just one day can expect an average premium increase of 17 percent. And a coverage lapse of 45 days or more costs New Jersey residents a premium increase of 35 percent.

See also: Bundling your insurance rates can save you up to 22% on premiums

It’s important to note most insurance companies will provide a 10-day grace period between the due date of your premium and a cancellation of the policy — although you’ll most likely have to fork over a late-payment fee, if you want to keep the coverage. This time frame may vary in states that require a slightly longer grace period, but don’t assume you’ll get one.

“Some of these findings are staggering, although I think the numbers are even more dramatic than this study shows,” says Doug Heller, an independent Los Angeles-based consumer advocate who specializes in the insurance industry. “But I don’t think most drivers give the issue of lapsed coverage a second thought until they are suddenly faced with a premium increase.”

What is a lapse in car insurance coverage?

A lapse in car insurance refers to the absence of coverage for any period longer than one day as a result of many factors, which typically include:

- The policy was canceled because you neglected to pay your premium.

- The policy was canceled because you caused an accident and your insurance company decided you are too risky to insure.

- The car insurance company went out of business.

- Your license was taken away, and you allowed the policy to lapse.

- You decided to no longer drive or own a car.

How will a lapse in coverage impact your premium?

Premium increases for a lapse in coverage will depend on a variety of factors, including how long you’ve gone without insurance and where you live.

Here are the states with the five most significant premium increases as the result of a one-day lapse in coverage:

1. Florida — 17 percent increase.

2. Arizona — 13 percent increase.

3. Connecticut — 13 percent increase.

4. Michigan — 13 percent increase.

5. Pennsylvania — 13 percent increase.

Meanwhile, here are the states with the five least significant premium increases from a one-day lapse in coverage:

1. California — No premium increase.

2. Texas — 2 percent increase.

3. New York — 2 percent increase.

4. New Mexico — 2 percent increase.

5. Massachusetts — 2 percent increase.

“A lot of these state-by-state differences come down to the (insurance) regulations of that particular state,” says Eli Lehrer, president of the nonprofit R Street Institute. “Often states that have larger increases for lapses will be states that try to suppress rates elsewhere. Insurers, for all intents and purposes, are ‘making up’ for it by raising premiums on lapsed policies. Also, there may be some differences in claims experience from state to state.”

The numbers start to change when the lapse is 45 days or longer. Here are the five states with the greatest premium increase as the result of a 45-day lapse in coverage:

1. New Jersey — 35 percent increase.

2. North Dakota — 28 percent increase.

3. Arizona — 26 percent increase.

4. Oregon — 22 percent increase.

5. Mississippi — 21 percent increase.

Meanwhile, here are the states with the five least significant premium increases as the result of a 45-day lapse in coverage:

1. California — No premium increase.

2. New York — 2 percent increase.

3. Massachusetts — 4 percent increase.

4. Delaware — 5 percent increase.

5. Maryland — 6 percent increase.

Why does a lapse in coverage result in a premium increase?

There are several reasons why a lapse in car insurance coverage may result in a premium spike, says Mike Barry, spokesman for the nonprofit Insurance Information Institute.

Generally speaking, Barry says letting a policy lapse raises the expense of underwriting that particular policy — a cost that is then passed on in the form of a higher premium.

“For starters, it costs more to process a new policy than a renewal on an existing policy,” says Barry. “And the run-up to the lapse has also probably cost the insurer money. For instance, in many cases an insurer has to notify the policyholder that a cancellation is eminent, and it costs money to process that paperwork.”

What’s more, Barry says actuarial data show that once someone has allowed a policy to lapse, he or she is more likely to lapse again in the future.

“Insurers have found that people who renew policies and don’t let them lapse are less likely to be in an accident, which means they are cheaper to insure,” says Barry.

But Heller is critical of this reasoning.

He acknowledges that some policies may lapse because of nonpayment or factors related to one’s driving record, but there are also many scenarios where a lapse in coverage may have nothing to do with financial delinquencies or errors behind the wheel.

“Often times a lapse has nothing to do with missing a payment, which means people are being punished for simply not having insurance. And that’s absurd,” Heller says.

See also: How car insurance claims affect rates (calculator)

California is the only state where a lapse in coverage — for any length of time — won’t result in a premium increase, according to the insuranceQuotes.com study. And this is because of a far-reaching state referendum passed several decades ago.

California voters passed Proposition 103 in 1988, a ballot measure that limited the factors insurance companies could use when determining auto rates. This included a ban on surcharges for drivers who were not previously insured or had had a lapse in coverage.

What can you do to avoid a lapsed-policy premium hike?

The most important thing consumers can do is explain to their insurance agent why a policy may lapse, according to Barry. For instance, if you plan to travel for a few months and won’t use your vehicle, call your insurer and explain before cancelling the policy. It’s possible you won’t be charged for a lapsed coverage when you reinstate the policy.

Another option is dropping liability and collision coverage and maintaining comprehensive coverage, Barry says. Comprehensive will cover events such as fire and theft.

“If you’re going to be driving, there is no reason not to have auto insurance. So make sure you are doing everything you can to maintain coverage while you’re on the road,” says Barry. “But if you’re not going to be driving and you don’t need insurance for a certain time, explain this to your agent before simply canceling the policy. Consumers can try to avert any misunderstandings by explaining upfront why there may be a lapse in coverage.”

Heller says it’s critical to shop around, whether your policy lapsed because of nonpayment or because you simply weren’t driving for an extended period of time.

“Shopping around will get you better prices, because every insurer is going to look at a lapse in coverage a little differently,” says Heller. “And when you’re shopping around, ask each company whether or not they are punishing you for a lack of prior coverage.”

Study methodology: insuranceQuotes.com commissioned Quadrant Information Services to measure the average economic impact of a lapse in auto insurance coverage. The study compared the average six-month premium increase for a lapse in coverage in all 50 states plus Washington, D.C.

Assumptions included: Driver is a 45-year-old married, employed female with a clean driving record. The hypothetical driver has a bachelor’s degree, an excellent credit score, no lapses in coverage and the following limits: $100,000/$300,000 (bodily injury), $100,000 (property damage), $100,000/$300,000 (UI/UIM), $10,000 (PIP) and a $500 deductible. The driver primarily drives one 2013 vehicle (a Toyota Camry, Honda CRV, Honda Civic, Ford F150 or Toyota Prius), including to work, 5 miles each way, with 12,000 annual miles. The study includes all available ZIP codes in each state.

- About the Author

- Latest Posts

Michael Giusti is a senior insurance analyst, business journalist, and university professor with over 20 years of experience. He serves as department chair at Loyola University New Orleans and contributes to Insurance Thought Leadership, U.S. News, and other leading financial outlets.

{kind=link}