How to File an Insurance Claim After a Hurricane

When a major hurricane is approaching the main concern for anyone in its path should be the personal safety of everyone in your family. Once the winds and rains have passed the next step is often planning a path for recovery.

And that path usually involves reaching out to their insurance company that provides hurricane coverage.

“Any time a customer needs to file a claim, it’s going to be emotional, but this is even more true during large disasters such as a major hurricane. It is at these times that customers want to feel connected to and taken care of by their chosen providers,” James Brown, CEO of enterprise customer communications management provider Smart Communications, tells the Insurance Journal.

“The way [customers] are communicated with has tremendous impact on this.”

RELATED: How Your Credit Affects Your Homeowners Insurance Rate

Of importance to policyholders is determining whether your home’s damage was due to floodwaters or from wind and/or driving rain.

What’s the difference? Well, it makes a big difference because flood insurance is a separate policy subsidized by the federal government that is not covered under a standard homeowners policy. Your insurance agent may have facilitated that purchase, but it is a separate policy with separate rules.

If rain came directly into your home, wind blew off a roof, or a tree fell on your house, then your homeowners policy will come into play. If you have yet to get home insurance for hurricane damage, you may want to start looking into different policies and comparing policies as soon as possible

Tips for filing claim after a hurricane storm

Hurricane victims, however, may not have the option of filing early, especially if it takes days to get back into their homes to assess the damage. Here are some tips for starting the claims process from the Insurance Information Institute.

- Make temporary repairs: Take reasonable steps to protect your property from further damage. Save receipts for what you spend and submit them to your insurance company for reimbursement. Remember that payments for temporary repairs are part of the total settlement. So if you pay a contractor a large sum for a temporary repair job, you may not have enough money for permanent repairs. Beware of contractors who ask for a large amount of money up front and contractors whose bids are very low — they might cut corners and do shabby work. Don’t make extensive permanent repairs until the claims adjuster has assessed the damage.

- If you need to relocate, keep your receipts: If you need to find other accommodations while your home is being repaired, keep records of your expenses. Homeowners insurance policies provide coverage for the cost of additional living expenses if your home is damaged by an insured disaster.

- Prepare for the adjuster’s visits: Your insurance company may send you a proof of loss form to complete or an adjuster may visit your home first. (An adjuster is a person professionally trained to assess the damage.) In either case, the more information you have about your damaged possessions — a description of the item, approximate date of purchase and what it would cost to replace or repair — the faster your claim generally can be settled.

History of hurricane and windstorm deductibles

If you live in a coastal region — or you’re thinking about buying property in a coastal state — here’s what you need to know about this unique and potentially expensive deductible.

“Hurricane deductibles help lower the cost of what people pay for property insurance on a year-to-year basis because they assume more of the risk,” says Lynne McChristian, Florida representative and catastrophe response director for the nonprofit Insurance Information Institute (III). “In other words you pay less today but more in out-of-pocket costs if a hurricane hits.”

CHECK OUT: What Is a Public Insurance Adjuster?

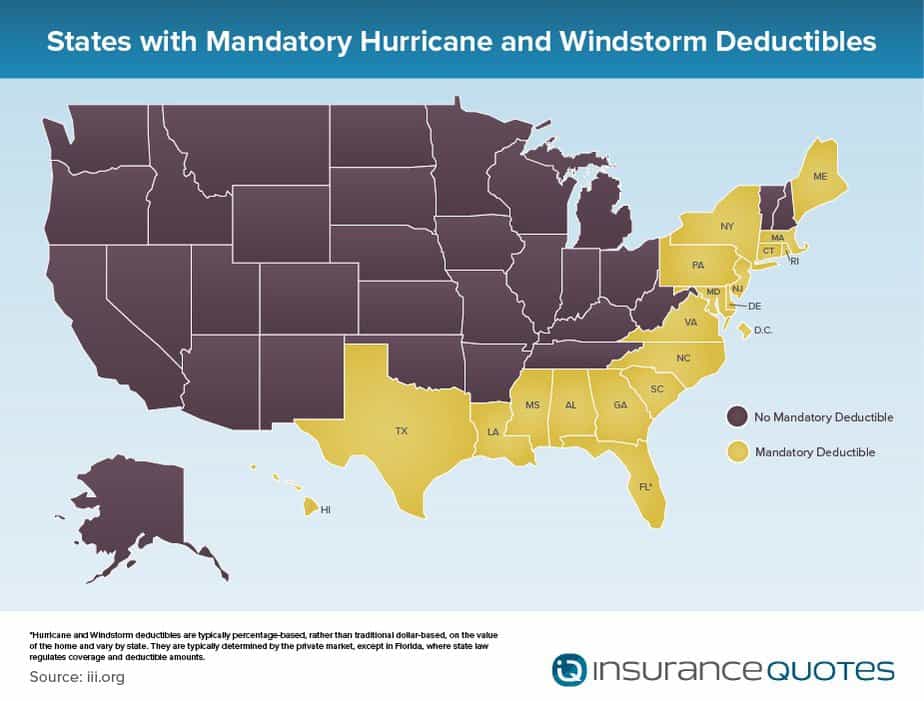

According to the III, hurricanes and tropical storms have caused $158.6 billion in insured losses between 1996 and 2015. In order to “limit their exposure to these losses,” insurers in 19 states and the District of Columbia now sell homeowners policies that include a percentage deductible that kicks in whenever a property experiences damage from a hurricane. It’s a separate deductible from all other potential perils like fire or vandalism and it has its own unique quirks and nuances.

The origins of hurricane deductibles can be traced back to Hurricane Andrew, which ravaged southern Florida in 1992 and left $15.5 billion in losses in its wake. It was the costliest hurricane in U.S. history until 2005, when Hurricane Katrina hit several Gulf States and cost insurers more than $41 billion in losses.

“Insured claims were so significant after Andrew that it prompted property insurers in coastal states to reassess how much damage a serious hurricane could actually do to their books of business,” says III spokesman Michael Barry. “It became clear that property owners had to assume more of the risk.”

As a result hurricane deductibles are now written into many coastal homeowner policies in the following 19 states: Alabama, Connecticut, Delaware, Florida, Georgia, Hawaii, Louisiana, Maine, Maryland, Massachusetts, Mississippi, New Jersey, New York, North Carolina, Pennsylvania, Rhode Island, South Carolina, Texas, Virginia and Washington, D.C.

“The bottom line is that property insurers feel like they need these deductibles in order to write policies in hurricane-prone states,” Barry says.

How hurricane deductibles work

Some specifics will vary depending on the state you call home, but Barry says most hurricane deductibles function the same way.

If your policy has a hurricane deductible and a named storm makes landfall in (and sometimes around) your state, you will have to pay anywhere between 1 and 5 percent of your home’s insured value before coverage for any damage kicks in. This is more costly than a standard $500 or $1,000 homeowners’ deductible, which kicks in for all other property losses.

For example, if your home is insured for $300,000 with a 2 percent hurricane deductible, you’d be responsible for the first $6,000 in repair costs for any damage caused by the storm.

It’s important to note, Barry says, that a hurricane deductible can only take affect if the home’s damage results from a storm officially named by the National Weather Service. The distinction, he says, is critical.

For example, when Superstorm Sandy hit the East Coast in 2012, the National Weather Service never officially designated it a hurricane because it lacked the sustained 75 mph winds necessary for that classification. As a result, homeowners in Sandy-hit states were not saddled with the additional financial burden of a hurricane deductible.

“The criteria for triggering a hurricane deductible is pretty specific,” Barry says. “So they don’t come into play all that often.”

States regulate rules for storm deductibles

Whether or not you’ll have to pay a hurricane deductible after a devastating storm is going to depend largely on the state you call home and the specific policy terms of your insurer.

“In other words,” Barry says, “not all hurricane deductible triggers are the same.”

For instance, New York’s Department of Financial Services has determined that a hurricane deductible (which is only applicable in eight of the state’s 62 counties) can be triggered either when a storm makes landfall as a Category 1 or higher anywhere in the state, or a hurricane makes landfall outside the state but causes losses to nearby New York properties.

What’s more, the state allows for a degree of trigger flexibility, which means some New York insurers trigger the deductible for a Category 1 storm while others use Category 2 as the threshold.

Florida, on the other hand, handles things a differently. For starters, hurricane deductibles and their requisite triggers are set by state law, which means all insurers must use the same trigger criteria.

CHECK OUT: Why Your Auto Insurance Claim Was Denied

What’s more, hurricane deductibles in Florida apply to any damage that occurs from the time a hurricane watch or warning is issued until 72 hours after the watch or warning ends. Importantly, the deductible can only be applied once each hurricane season, which falls between June and November.

Finally, not all homeowners living in hurricane deductible states will shoulder the financial burden of this provision. For instance, mandatory hurricane deductibles in New Jersey can only be applied to ZIP codes specified by state law and areas approved by the New Jersey Department of Banking and Insurance.

“All of these variables are based on what’s needed to maintain a healthy insurance market in hurricane-prone areas of the country,” McChristian says. “Insurers need to be able to price a policy that is affordable, and that’s going to look different in coastal Florida than, say, inland New Jersey.”

For a comprehensive breakdown of state-by-state hurricane deductible rules and regulations check out this extensive page from the III.

Are hurricane deductibles fair?

While the insurance industry touts hurricane deductibles as a financial necessity for policies written in hurricane-prone regions, some consumer advocates say the practice is unfair.

“Insurers will say that you’re living closer to harms way and therefore you should bear a greater share of the risk, but I don’t see these deductibles as a fair way of doing that,” says Amy Bach, executive director of United Policyholders, a San Francisco-based nonprofit that advocates for insurance consumers in all 50 states. “Homeowners in these coastal areas are already paying higher insurance rates for living there, which means hurricane deductibles are like a double penalty.”

Indeed, hurricane-prone coastal states are traditionally some of the most expensive for homeowners insurance.

For instance, according the National Association of Insurance Commissioners (NAIC), Florida residents pay, on average, $2,055 per year for home insurance, making it the most expensive home insurance state in the country. Second and third on the list are Texas and Louisiana, which are also hurricane-deductible states.

RELATED: 6 Surprising Exclusions to Your Homeowners Policy

“I don’t like insurers using deductibles this way. The reason people buy insurance is so they have access to funds for repairs when something bad happens. All a hurricane deducible does it make it harder to do that,” Bach says. “In my opinion, having these high hurricane deductibles undermines the value of the product to the consumer. And it doesn’t bring prices down as much as it should. The consumer just doesn’t see a sufficient benefit.”

Know your storm deductible and be prepared

Hurricane season is fast approaching, which means that if you live in any of these 19 states you need to know the specifics of your hurricane deductible and understand the financial implications of filing a claim should a storm hit.

The good news is that in most states it’s easy to find out if you have a hurricane deductible and how it might be applied. For instance, insurers in Delaware are required to provide “clear and prominent notice concerning all hurricane and wind/hail deductibles and must include information on the trigger, how the deductible is applied, and if it is stated as a percentage or dollar amount.”

In Florida, state law dictates that hurricane deductibles be identified with the following statement written in bold, 18-point type on the policy’s declarations page: “This policy contains a separate deductible for hurricane losses, which may result in high out-of-pocket expenses to you.”

Once you determine if this deductible applies to your home, McChristian suggests making a financial plan well in advance of a potentially devastating storm.

“Don’t be caught off guard. People should take this hurricane season to understand the specific dollar amount of their deductible if they ever file a claim after a hurricane,” McChristian says. “They’re saving money on their premium every year, so take those savings and set some money aside in a deductible fund that you can tap into if need be.”

Editor’s Note: This article has been updated from the original version published in 2018.

- About the Author

- Latest Posts

Autumn Cafiero Giusti is a licensed life and health insurance broker and award-winning journalist with more than 20 years of experience. She writes extensively about flood, Medicare, home, and life insurance for publications like U.S. News and CBS News.