Guide to Marijuana Use and Insurance for 2019

Check out our updated Cannabis Insurance Report for 2021 for updates on the issues discussed here.

The past decade has been undeniably transformative for U.S. marijuana laws. Not since the era of Prohibition has the United States wrestled so broadly and intensely with the cultural, judicial, and economic implications of legalizing a formerly illegal substance. And while the push to reform state marijuana laws continues sweeping the country with unambiguous fervor — a late-2018 Gallup poll showed 64 percent of Americans favor legalization — many questions and complications remain.

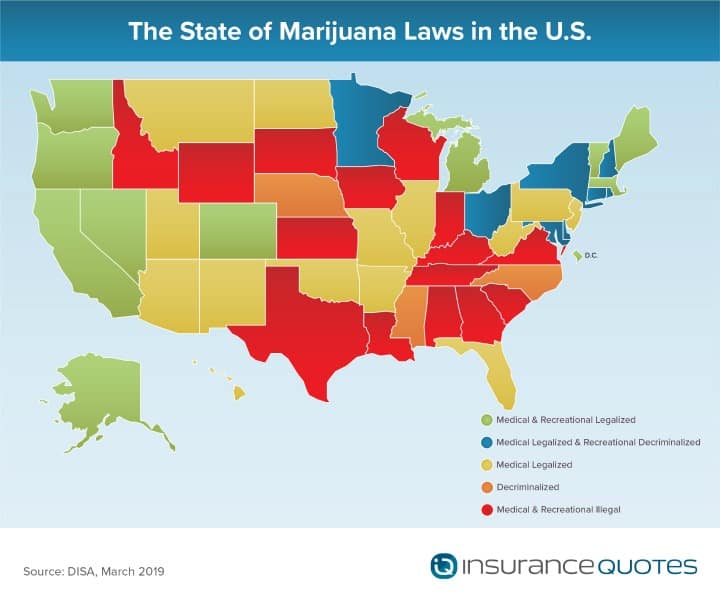

To date, 33 states and the District of Columbia have legalized medical marijuana, and 11 states — Alaska, California, Colorado, the District of Columbia, Massachusetts, Maine, Michigan, Nevada, Oregon, Vermont, and Washington — have legalized the use of recreational marijuana for adults over 21.

What’s more, New York, New Jersey, Connecticut and Illinois are poised to pass legalization legislation in 2019, while movements to get a legalization initiative on the ballot in 2020 are underway in Arizona and Ohio.

Whether it’s being used as medicine or for leisure, the swift-moving marijuana legalization trend has resulted in myriad state laws that conflict with the federal government’s official position on the production, possession, and consumption of cannabis. What’s more, the particulars of individual state laws are anything but uniform, and what’s considered legal in one state may be unlawful in another — even if they both allow for some degree of marijuana possession or consumption.

As a result, the insurance implications are as varied as they are complicated.

“The insurance industry has run into an interesting area where they know marijuana is legal in some states but that it’s also not legal according to federal law. And that’s led to a real insurance quandary,” says Brenda Wells, director of the risk management and insurance program at East Carolina University in Greenville, North Carolina. “Do they cover it? Do they not cover it? And if they do cover it, how is it valued? These are just some of the questions they’re wrestling with at this stage. And it can get confusing.”

To help navigate these muddy waters, insuranceQuotes offers some key considerations for marijuana’s impact on various components of the insurance industry.

Marijuana and homeowners insurance

The question is simple: If you have some marijuana and it’s damaged in a fire or stolen from your property, will your homeowners insurance policy cover the loss?

The answer, however, is not so straightforward.

To begin with, the federal government still considers cannabis an illegal substance under the Controlled Substances Act (CSA), which classifies it as a Schedule I drug and is stated “to have no currently accepted medical use in treatment in the United States.”

Despite the fact that the majority of U.S. states have some form of marijuana legalization on the books, this federal classification continues to make insurers wary of covering marijuana-related losses for policyholders. What’s more, most homeowner policies have explicit exclusionary language related to controlled substances, which means that a claim for lost, stolen, or vandalized cannabis may be denied if the insurer believes the loss falls within the exclusion.

“Marijuana presents a very unique risk from an insurance standpoint,” Wells says. “Not only do you have increased risk for things like fire and theft, but you also have this pervasive anxiety about covering losses for a federally banned substance. A lot of companies are reluctant to even talk about it. In general, the industry hasn’t been handling this very well, but they need to figure out if they’re going to cover this. And if they are, they need to be prepared to pay claims like they would for anything else.”

Trying to find a catchall approach to the marijuana home insurance quandary produces a staggering variety of anecdotes, opinions, and legal vagaries that fluctuate from state to state and from insurer to insurer. At the end of the day, whether a loss is covered or not will most likely be up to the individual insurer.

RELATED: Raise Your Deductible to Lower Homeowners Insurance Premiums

“Legal marijuana is one of a few Wild West issues facing property insurance right now. It’s vast, uncharted territory,” says Janet Tulsette, a Connecticut-based property insurance consultant who has recently specialized in the intersection of insurance and marijuana law. “Not only is it complicated because every state handles the substance differently, but it’s also so unprecedented, which means insurers are reluctant to be the first to make any bold moves one way or the other. They’re playing it relatively safe, but that makes things more complicated, not less.”

As of right now some insurers are looking to individual state laws to establish a precedent for coverage. For instance, Allstate went on the record in 2014 saying it would cover the loss of marijuana in Colorado, where cannabis is legal for both medicinal and recreational use.

“In Colorado, lawfully possessed, processed marijuana is not excluded and is limited to the personal property limit of the homeowners policy,” Allstate said in a statement that year. “Whether it is medical or non-medical is not relevant to coverage. Fire is a covered peril, and coverage of an accidental fire would not be impacted by whether or not it was started in connection to lawful marijuana use.”

They added that marijuana plants grown with a state license — and not exceeding the legal state limit — would be “limited to the perils and limits under additional protection for trees, shrubs, plants and lawns.”

But, says Wells, this does not address the more perplexing problem of marijuana’s monetary value and conflicts between state and federal laws — a specific sticking point that has hamstrung the evolution of marijuana insurance for the past decade without any clear signs of future alleviation.

“Even if insurers are writing policies in line with state laws, there’s the critical problem of valuation,” says Wells, who is currently working on an update to her seminal 2014 paper title Marijuana Legalization: Implications for Property/Casualty Insurance. “It’s incredibly hard to establish a market value for marijuana across the board, and how this is handled is going to vary from state to state.”

For instance, a federal court in Hawaii ruled in 2012 that a homeowners policy did not cover the theft of one woman’s marijuana plants grown for medicinal use.

The homeowner, Barbara Tracy, was allowed to grow and possess marijuana for her own medical use, and after 12 plants were stolen she submitted a claim to USAA for $45,600. USAA initially agreed to pay Tracy $8,801 for the claim, but Tracy sued, claiming the plants had a far greater value.

USAA argued that because marijuana is federally classified as an illegal Schedule I substance (akin to heroin, morphine, and LSD) they were under no obligation to cover the loss at all. The court ultimately agreed with USAA, stating that even though Hawaii law permits the use of marijuana for medicinal use it is illegal under the Controlled Substances Act and therefore not subject to homeowners’ insurance coverage.

“That Hawaii case remains the most highly-publicized collision of marijuana and home insurance,” Tulsette says. “And I think a lot of large insurance providers are wary of getting their names in headlines for similar issues.”

Some states are pre-emptively combatting these types of conflicts by including language in marijuana legalization laws that prevents insurers from denying claims like Tracy’s.

For instance, Oregon’s Control, Regulation and Taxation of Marijuana and Hemp Act states, “No contract shall be unenforceable on the basis that manufacturing, distributing, dispensing, possessing or using marijuana is prohibited by federal law.”

In other states, possession limits are so low that insurance companies aren’t bothering to fight claims.

For instance, Wells points out that Connecticut allows for the possession of up to 2.5 ounces of “useable marijuana” for medicinal purposes.

“If 2.5 ounces were stolen or lost in a fire, the value of that loss would probably be less than $1,000,” Wells says. “And an insurance company isn’t going to go to the mat over such a small claim.”

Nonetheless, there is a lot of money at stake here on the whole. According to Fortune, the United States’ legal marijuana industry grew to $10.4 billion in 2018 (it was $6.5 billion in 2016) and employed more than 250,000 people. What’s more, Fortune estimates that investors will “funnel more than $16 billion into the industry” in 2019.

“The industry is only going to grow, and the losses associated with legal marijuana are only going to increase,” says Tulsette. “The insurance industry really needs to come up with comprehensive and substantive solutions. They can only keep their heads in the sand for so long.”

Marijuana and life insurance

As more and more Americans legally smoke cannabis for recreational and medicinal use, life insurance providers have had to grapple with its impact on the application and underwriting process.

According to insurance specialist Michael Quinn, life insurance providers are wrestling with whether or not smoking marijuana carries the same health risks as smoking cigarettes.

“Regular smokers are charged tobacco rates, which are often four times higher than those for non-tobacco users,” Quinn says. “But some insurers are deciding to treat marijuana differently.”

CHECK OUT: Health Care at Any Cost?

For instance, Prudential tends to offer some of the lowest life insurance rates for marijuana users because they do not place them in the same risk pool as cigarette smokers. According to Prudential, a preferred non-tobacco rate is granted to users who smoke marijuana no more than three times per week, and insurance applicants must admit to marijuana use during the application process.

Meanwhile, providers like United of Omaha offer non-tobacco rates for those who smoke marijuana no more than three times per month, while John Hancock stipulates that it considers smoking marijuana “drug use” and will not offer applicants competitive rates.

“Based on your marijuana use alone, there is no telling what kind of rates you will be offered. You could technically get rates anywhere from substandard to preferred plus,” Quinn says. “However, a company like Prudential looks at the reason behind your marijuana use, and if it’s for medicinal reasons your rates will be based on the severity of your health condition, not the marijuana use alone.”

For instance, let’s say a hypothetical man named Jim smokes medical marijuana to help with insomnia. As a 50-year-old in otherwise perfect health, Prudential would offer him a preferred plus non-tobacco rate.

If, however, Jim uses medicinal marijuana to ease the symptoms of multiple sclerosis, he would get a higher rate based on the severity of the condition being treated, not his use of marijuana.

Nonetheless, the extent to which your life insurance might be affected by smoking marijuana will depend on the individual insurer and the frequency of your use.

“For underwriting consideration, the first thing we must determine is whether the use is recreational, or if the proposed insured had been issued a prescription for medical use,” says Pinney Insurance underwriter Mike Woods. “If it’s for medicinal purposes, underwriting is going to be looking to the specific issue that the marijuana is being used to treat.”

For recreational use, Woods says the underwriter is going to want to know the frequency of use and the legality of that use in the state you call home.

“Cannabis contains carcinogens, and evidence suggests that heavy cannabis use may be associated with oral cavity, pharynx, esophageal, and lung cancers,” Woods says. “Because of those concerns, many carriers will assign tobacco use rates for any use.”

Marijuana’s impact on businesses

For businesses in the legalized marijuana industry, insurance providers are still operating in unchartered waters, says Tim Davis, workers compensation and general liability insurance expert.

“Because marijuana is still against federal laws, this causes a major limitation in the marketplace for any business that serves or operates in the marijuana industry,” Davis says. “General liability exposure is still untested, and since the exposure is too new to have time to develop, we will have to see how the premiums for this industry shake out.”

CHECK OUT: These Insurance Misconceptions Can Put You At-Risk

For instance, if you own a marijuana retail store and someone falls while shopping there, general liability insurance would cover any medical costs incurred by the shopper. What’s more, product liability issues may come into play for marijuana retailers selling edible marijuana food products.

To be sure, the need for a comprehensive approach to insuring various aspects of the marijuana industry is becoming increasingly critical for everyone from growers to dispensary owners, and there are signs that the insurance industry is starting to pay attention.

“Cannabis-related businesses (CRBs) face many risks and obstacles. Some of the biggest risks involve theft, general liability and product liability,” wrote the National Association of Insurance Commissioners (NAIC) in an official statement from late 2018 addressing the industry’s shortcomings in this space. “Companies functioning within state legality face severe banking restrictions due to federal regulations. CRBs may be forced to handle large sums of cash, subjecting them to a higher risk of theft. CRBs share the same general liability and other risks agricultural and manufacturing businesses face. This includes workplace accidents, damage to property, and crop failure. CRBs are especially prone to fires from both wild and internal sources.”

“Things are definitely going to look different in another five years or so, but right now so many marijuana business owners are working without a harness or safety net,” says Anthony Bonfiglio, a Colorado-based lawyer who specializes in marijuana law. “That means they have to be fearful of everything from crop fires to business theft, liability, or vandalism. It’s a stress that no other industry has to bear, and it’s unsustainable in the long term.”

As of right now, many of the big-name insurers are explicitly steering clear of providing business insurance for marijuana-related ventures, including Allianz SE, Nationwide Mutual Insurance Co., and Hartford Financial Services Group Inc., which said it is abstaining from the marijuana industry and “is unlikely to change” while the federal ban is in place. “We do not underwrite any business that sells, grows, transports or distributes marijuana or products derived from marijuana cannabinoids,” the company said in an official statement from late 2018.

But even as the insurance industry continues showing broad reluctance to write policies aimed at protecting marijuana-related businesses from financial loss, some states are taking a more proactive regulatory approach to solving the myriad quandaries that have arisen due to the collision of legalized marijuana and the insurance industry.

For instance, California Insurance Commissioner Dave Jones announced in June 2017 the approval of the first Cannabis Business Owners Policy (CannaBOP) in California. The program provides property and liability coverage for dispensaries, processors, manufacturers, distributors, cannabis storage facilities and other relative businesses operating in the state.

“My objective is anytime a consumer walks into a cannabis retail facility or a vendor enters into a contract or delivers goods to a cannabis business, or anytime someone invests in or operates a cannabis business, insurance is in place to cover risks,” Jones said in a recent phone interview with Forbes, “just as there is in any other form of business in California.”

Jones also approved California Mutual Insurance Company as the first provider in the state to offer insurance to retail landlords who rent to commercial cannabis industry tenants. According to Forbes, the policy provides “liability and property insurance for commercial property owners who lease building space for cannabis labs, product manufacturing, cultivation, and dispensary operations.”

Finally, as large insurers continue to sidestep the marijuana industry, smaller carriers and subsidiaries have begun trying to fill the gap.

For instance, Brown & Brown Insurance now offers marijuana business insurance through a new company division called Cannabis Insurance Professionals (CIP), which is based out of California but licensed in all 50 states. CIP garnered national headlines last year after the company paid out more than $1 million to one of its clients whose marijuana crop was destroyed in the 2018 Thomas wild fire.

“Premiums are still incredibly high for the small carriers who offer insurance to the marijuana industry because no one knows yet if this type of insurance will be profitable,” says Davis, who believes we will slowly see more insurers like CIP entering the market over the next five years. “There’s still no standard to follow across the board.”

Assuming the national trend for marijuana legalization continues, Bonfiglio believes this will change rapidly over the next five-to-10 years as courts and governments address some of the key coverage concerns and conflicts between state and federal law.

“We may have to endure a few more years of timidity and confusing state-by-state laws and regulations, but eventually the scale is going to tip,” says Bonfiglio. “Whether that means federal legalization or just a tidal wave of states, insurance companies are going to get on board with providing adequate business insurance. After all, there’s a lot of money to be made in this industry, and insurers definitely want a piece of the pie.”

Marijuana and auto insurance

The intersection of legal marijuana and auto insurance has been fairly uncomplicated thus far, and that’s because the insurance ramifications for getting caught driving high are no different than those associated with driving under the influence of alcohol.

“If you’re convicted of driving under the influence of marijuana your insurance rates will go up, just like they would if you were charged with a traditional DUI for booze,” Wells says.

RELATED: What’s Worth the Risk of a Traffic Ticket?

However, one of the most significant questions concerning legalization is whether or not more recreational pot legalization has led to more incidents involving so-called drugged driving.

According to a recent study conducted by the Insurance Institute for Highway Safety (IIHS) and Highway Loss Data Institute (HLDI), motor vehicle crashes are up six percent in four states that have legalized recreational marijuana — Colorado, Nevada, Oregon, and Washington — compared with four neighboring states where the drug is restricted or illegal.

In an official statement, IIHS and HLDI president David Harkey said, “What we’re seeing is a definite increase in crash risk that is associated with the legalized recreational use of marijuana,” but cautioned that “the study results indicate only a correlation between marijuana legalization and a higher number of crashes,” adding that “more research would be necessary to determine whether marijuana use caused the increase.”

“I would say the legalization of marijuana has caused a spike in auto accidents for a few reasons, and the most significant one is that new users who don’t have any tolerance to marijuana often overuse it and are not aware of its effects until it’s too late,” says Lindsey Parlin, a Colorado-based criminal defense attorney who specializes in DUI cases. “Even if you smoked 30 years ago, you might not realize that the effects of the marijuana out there today are much more significant.”

Nonetheless, it’s very difficult to find any empirical data that links marijuana legalization to an increase in stoned driving in any of the 11 states that now allow for its recreational use.

“A big problem is that there is no separate DUI law for driving under the influence of marijuana,” says Sam Tracy, former chairman of the international nonprofit Students for Sensible Drug Policy. “They just sort of wrap it into the alcohol laws, so if you get charged with a DUI we don’t have data that splits out marijuana versus alcohol versus prescription drugs … so we haven’t been able to get a solid understanding of the effects of legalization.”

Still, there are some who urge a great deal of caution despite the lack of data.

“With the higher prevalence of marijuana in the world, what we’re seeing is a sort of denial of the fact that marijuana can be impairing,” says Chris Cochran, spokesperson for California’s Office of Traffic Safety. “Marijuana is not a benign substance when it comes to driving ability. It throws off your perception of time, loosens inhibitions, and changes reaction times. We can’t just say, ‘Oh, people who are high drive slower and nicer.’

“Anything you put into your body that will alter your brain chemistry is potentially impairing and dangerous behind the wheel.”

Medical marijuana and health insurance

Even if you live in one of the states that have legalized marijuana for medicinal use, don’t expect your health insurance to foot the bill.

Because of its federal designation as a Schedule I controlled substance, health insurance providers have their hands tied when it comes to reimbursing patients using medicinal cannabis, says Wells.

What’s more, marijuana is not an approved medical treatment by the FDA, and because of its Schedule I classification extensive clinical research on its medicinal efficacy has been difficult to obtain.

“That probably isn’t going to change anytime soon,” Wells says.

Editor’s note: This is an updated version of an article originally published in April 2017.

- About the Author

- Latest Posts

Autumn Cafiero Giusti is a licensed life and health insurance broker and award-winning journalist with more than 20 years of experience. She writes extensively about flood, Medicare, home, and life insurance for publications like U.S. News and CBS News.