Get Free Home Insurance Quotes — Compare Top Carriers in Minutes

Homeowners insurance averages $2,490 per year ($207 per month) for $400,000 in dwelling coverage nationally in 2026, based on InsuranceQuotes.com’s rate analysis. USAA offers the lowest rates for military families; Amica Mutual and State Farm are consistently among the most competitive carriers for standard policyholders. The most critical pricing factor: your home’s rebuild cost — not its market value — combined with your claims history and location.

At Insurance Quotes we’ve helped homeowners save on home insurance since for 18 years. Fill out our fast and simple form to compare the best local and national home insurance companies – all in one place.

We give you the tools to easily compare multiple homeowners insurance quotes all at once. With an A+ BBB rating we help over 30K+ people a day find the best home insurance rates with policies that cover all of your home coverage needs. We can help you keep one of your biggest investments – your home – covered with multiple policy options to choose from.

Do I Need Homeowner’s Insurance?

Homeowner’s insurance isn’t required by law; however, if you have a mortgage on your home then the lender will most likely legally require you to have an insurance plan that insures 100% of the home’s replacement cost until your home loan is paid in full. If you currently own your home you are technically not required to have home insurance coverage by law. For most homeowners however, having home insurance coverage is a no-brainer as it insures you can avoid substantial financial loss to one of your greatest assets should something happen to it.

If you were to experience a situation where your home was destroyed as well as all of your personal belongings, for most this would be an incredibly challenging financial situation to recover from. The benefit of knowing your home and belongings are insured can be a great peace of mind even for those who have fully paid off their home’s mortgage.

Explore Home Insurance Costs by State and City

Home insurance rates can vary dramatically depending on where you live. Comparing average rates by state and city helps you understand what’s normal in your area, identify potential savings, and avoid overpaying. Whether you’re moving, buying your first home, or reviewing your current policy, these location-based guides provide actionable data and insights to help you make confident decisions.

The following city-level guides provide real-time home insurance cost data, local market trends, and insights tailored to each ZIP code. Whether you’re buying a home or renewing your policy, these resources help you make more informed decisions.

These state-level guides offer a broader view of home insurance pricing and coverage factors across entire regions. You’ll find comparisons by provider, disaster risk zones, and policy types to help you better understand where your state fits into the national average.

Data sources: Quadrant Information Services (real-time rate data), publicly available insurer filings, and proprietary quote form data from InsuranceQuotes.com (2025).

What Does House Insurance Cover?

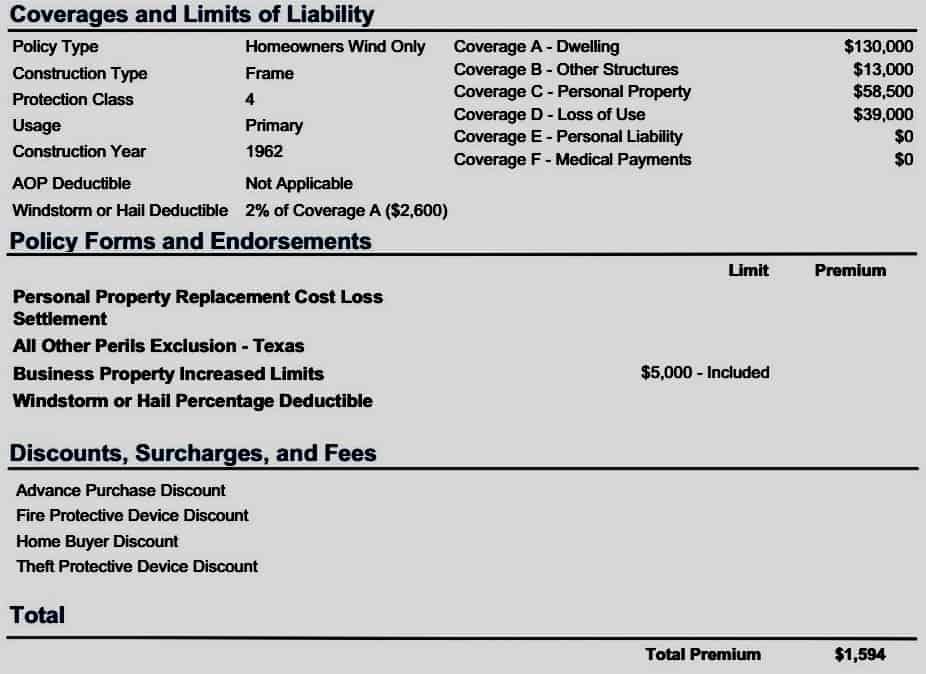

Home insurance coverage can vary from plan to plan. The most common events that you will be covered from under a homeowner insurance policy include protection from property damage such as fire, lightning strike, hurricanes, wind storms, hail storms, and water damage (usually from busted pipes). Some natural disaster damages are not included under a regular policy such as earthquakes, mudslides, and flood damage. Below is an example of a home insurance quote:

Dwelling insurance covers any damage to the home or attached building structures such as a garage or home’s front porch.

Personal Property:

Personal property liability covers paying for replacement or repairs to any belongings that are damaged and or stolen in certain events covered under your policy.

Other Structures:

This coverage takes care of any other structures that are stand-alone detached entities on your land such as a tool shed, fence, pool, or mailbox.

Liability:

Personal liability reimburses you for any legal action taken on you for accidental injury or property damages to others that occur on your property.

Additional Living Expenses (ALE):

ALE coverage reimburses the costs associated with being displaced from your home such as temporary lodging, food purchase, and other living expenses occurred when your home is unavailable to live in.

Medical Payment:

Medical payment coverage protects against any costs of minor injuries that someone not living on the property sustains while visiting.

What is the average cost of homeowners insurance in 2026?

The national average is approximately $2,490/year for $400,000 in dwelling coverage in 2026 (~$207/month). Rates vary dramatically by state: California averages $1,641/year while Florida averages $5,838/year for a $300,000 dwelling. Amica, USAA, and State Farm consistently offer the lowest rates among major national carriers. Your exact rate depends on your location, home age, construction type, and credit score.

What is the 80% rule for home insurance?

The 80% rule states you should insure your home for at least 80% of its full replacement cost to receive full claims coverage. If your $500,000 rebuild-cost home only has $300,000 in coverage (60%), your insurer may pay only a proportional share of any claim. In practice, most major insurers now require 100% replacement cost coverage — not just 80% — using their own rebuild-cost calculators. The 80% figure is a floor, not a target.

How much is home insurance on a $400,000 house?

Expect to pay approximately $2,490/year ($207/month) nationally in 2026 for $400K in dwelling coverage. Your credit score significantly affects your rate in most states — homeowners with excellent credit can pay up to half as much as those with poor credit for identical coverage. Raising your deductible from $1,000 to $2,500 typically saves about 9% on your premium. The fastest way to find your specific rate: compare quotes from multiple carriers at once on InsuranceQuotes.com.

Does home insurance cover flooding?

No — standard homeowners insurance does not cover flooding. Flood damage requires a separate policy through FEMA’s National Flood Insurance Program (NFIP) or a private flood insurer. Average NFIP flood insurance costs approximately $888/year nationally. Homes in FEMA flood zones with federally-backed mortgages are required to carry flood insurance. Check your flood zone at msc.fema.gov. If you’re in a high-risk zone, flood insurance is not optional — it’s required by your lender.

What does homeowners insurance not cover?

Standard home insurance (HO-3) does NOT cover: flooding (requires separate NFIP/private policy), earthquakes (requires a rider or standalone policy), normal wear and tear, pest infestations (termites, rodents), sewer backup without an endorsement, or intentional damage. Home-based business liability and equipment typically require a separate business rider. Always review your policy’s exclusions section and ask your agent about coverage gaps specific to your ZIP code — especially weather risks.

How many home insurance quotes should I get?

Get at least 3 quotes, ideally 5 or more. Home insurance rates can vary by several hundred dollars per year for identical coverage. Rate variation between major carriers for identical coverage can exceed $1,200 annually. InsuranceQuotes.com lets you compare quotes from top carriers — USAA, State Farm, Erie, Allstate, Travelers, and more — with a single form. Free, no spam, takes 2 minutes.

2026 Average Home Insurance Rates by Carrier

For a $300,000 dwelling policy · InsuranceQuotes.com 2026 rate analysis · Rates are market averages and will vary by location, home, and profile

Carrier

Avg. Monthly

Avg. Annual

Best For

USAACheapestMilitary only

$149

$1,788

Military families & veterans

Amica MutualLowest rates overall

~$150

~$1,800

High customer satisfaction

State Farm

~$155

~$1,860

Nationwide availability

Erie InsuranceNortheast/Midwest

~$160

~$1,920

Claims satisfaction, regional

Shelter InsuranceMidwest/South

~$163

~$1,956

Competitive in Midwest/South

Allstate

~$180

~$2,160

Wide coverage options

Progressive

$215

$2,580

Bundling, high deductibles

Rates shown for $300K dwelling, $100K liability, good credit. USAA available to military/veterans only. Regional carriers (Erie, Shelter) may not be available in your state.

What Factors Determine My Homeowners Insurance Costs?

House age and materials used: The older your house, the higher the risk of losses or damages from general deterioration or from external factors like harsh weather conditions. Houses made of lightweight materials, like wood, will be more likely to get damaged than houses made from brick, stone or cement. The state of the roof on your house needs to be considered too because if replacement or repair is needed, the costs of labor and materials increase with time.

Home security: Having an efficient home security system in your house has a two-fold effect – it can reduce your insurance premium while also giving extra protection to your family and your possessions against theft and vandalism. Updating the locks in your home can help in reducing the cost of your premium, as can installing fire alarms or sprinkler systems.

House renovations:If you have done or started any renovations to your home, you have added value to your home. Some renovations that add value include updating pipes or adding additions. Make sure you advise your homeowners insurance provider as these new improvements need to be accounted for in your policy and premium rates.

Home Location:If your home is in an area that is prone to natural disasters you can expect to pay a higher premium from the risk associated with that location. You may also want to check out if your ZIP code carries higher premiums. ZIP codes with higher numbers of theft claims, for example, could hike your insurance premiums up 3-5 percent.

There are many factors to consider when thinking about home insurance. Getting the right information and putting together a personalized, affordable plan for your home can only be done by the experts. It only takes a few minutes of your time to get your free homeowner’s insurance quote. Contact us today to compare multiple insurance quotes or chat about your options.

Last updated: June 26, 2025 Brian is a veteran financial journalist and best-selling author with over two decades of experience covering insurance, personal finance, and Wall Street trends. He contributes regularly to major publications and helps ensure our content meets high standards of accuracy, clarity, and relevance.

World Cup 2026 Insurance Guide: How the biggest sporting event in North America is protected By Michael Giusti When the FIFA World Cup kicks off on June 11, 2026, it will be much more than a soccer tournament. Spanning more than five weeks and hosted across the…

Memorial Day weekend is the unofficial start of summer, and it is one of the busiest travel and hosting weekends of the year. Whether it’s a road trip, a flight across the country, or a backyard barbecue with friends and family, the long weekend comes with a…

It could be a staged accident, or it could be misinformation on an insurance form. Either way it is insurance fraud. Insurance fraud is widespread, costly and sometimes easier to commit than consumers realize. It affects nearly every policyholder through higher premiums, more difficult claims reviews and…

Weddings are one of the most significant financial and emotional investments many couples will ever make. Between the venue, catering, attire, travel, and everything in between, the cost of a modern wedding can rival that of a car, or even a down payment on a home. That…

What is the Average Monthly Cost for Home Insurance?

Home insurance costs will vary depending on a many factors. On average you can expect to pay around $328 a month or $3,942 a year for a 3 bedroom updated home in a rural area.

Is Homeowner’s Insurance Required?

Though homeowner’s insurance is not required legally by any state, if you have a mortgage through a bank or lender – you will always be required to have house insurance on the property.

What Does Home Insurance Cover?

A standard home insurance policy will usually cover things like damages or destruction of a home including interior and exteriors, a loss due to theft, and liability if someone is harmed on your property. There are additional coverage options for different property types.

What Information Do You Need to Get a Free Home Insurance Quote?

Getting a free home insurance quote online takes about 5–10 minutes. Here’s exactly what information you’ll need to have ready to get the most accurate quote:

Your home’s address and year built. Location determines flood zone, fire protection class, and neighborhood risk. Year built affects wiring, plumbing, and roof age — all key pricing factors.

Square footage and construction type. The size of your home and whether it’s wood frame, masonry, or mixed construction directly affects the rebuild cost estimate that sets your dwelling coverage limit.

Roof type and year last replaced. Insurers price heavily on roof condition. A roof over 20 years old can add 10–25% to your premium or trigger a coverage requirement. Know when your roof was last replaced and what material it uses (asphalt shingle, metal, tile).

Your desired coverage levels. You’ll need to decide on dwelling coverage (rebuild cost — not market value), personal property coverage, liability limit ($100,000 minimum, $300,000 recommended), and deductible ($1,000 or $2,500 are most common).

Claims history for the past 3–5 years. Insurers will check your CLUE (Comprehensive Loss Underwriting Exchange) report. Being upfront about prior claims saves time.

Current insurer (if applicable). Many carriers offer loyalty discounts for switching before your policy lapses, or competitive new customer rates for switching from a named competitor.

Your Social Security Number (optional but helpful). Most states allow credit-based insurance scoring, which can significantly affect your quote. Only California, Hawaii, and Massachusetts prohibit credit scoring for home insurance.

How to Compare Home Insurance Quotes — And What to Actually Compare

Getting multiple free quotes is only valuable if you’re comparing the right things. Most homeowners focus only on the annual premium — but this approach often leads to being underinsured or surprised at claims time. Here’s what to actually compare:

Dwelling coverage vs. your home’s rebuild cost: Make sure every quote uses the same dwelling coverage limit — ideally your home’s actual replacement cost (what it costs to rebuild, not what it would sell for). An appraisal or contractor estimate can establish this. Quotes set at different dwelling values aren’t comparable.

Replacement cost vs. actual cash value: Replacement cost coverage pays to replace your belongings at today’s prices. Actual cash value pays the depreciated value of a 10-year-old couch. Always choose replacement cost if available — the premium difference is small, the claims difference is huge.

Deductible: A $500 deductible vs. $2,500 deductible can mean $200–$500 difference in annual premium. A higher deductible lowers premium but means more out-of-pocket in a claim. For most homeowners, a $1,000–$2,500 deductible hits the right balance.

Liability limit: The standard $100,000 liability limit is often insufficient. For homeowners with significant assets — a retirement account, home equity, savings — $300,000–$500,000 in liability is recommended. Umbrella policies extend liability for $150–$300/year additional and provide $1M+ in coverage.

Excluded perils: Standard policies exclude flood, earthquake, and sewer backup. If your location warrants coverage for any of these, factor in the cost of a separate rider or policy when comparing total insurance costs.

InsuranceQuotes displays side-by-side quotes from multiple carriers so you can compare apples to apples. Fill out one form to see rates from State Farm, Allstate, Travelers, and other top providers in your area instantly — no spam, no obligation.

Autumn Cafiero Giusti is a licensed life and health insurance broker and award-winning journalist with more than 20 years of experience. She writes extensively about flood, Medicare, home, and life insurance for publications like U.S. News and CBS News.