Millennials are confident about financial health but are underinsured

Generation Y is underinsured, and nearly 1 in 4 millennials lacks health insurance despite the federal law that requires all Americans to get covered, a new survey shows.

The survey from Princeton Survey Research Associates International, commissioned by insuranceQuotes.com, found that 24 percent of consumers ages 18 to 29 don’t have health insurance. In contrast, only 12 percent of over-30 adults lack health insurance.

And it’s not just health insurance where Gen Y falls short: Millennials were least likely of any age group to have any type of insurance, including auto, renters or homeowners insurance, life, and disability, or health insurance coverage according to the survey.

Why are millennials underinsured?

Youth is part of the reason Gen Y buys less insurance, says Kile Lewis, co-CEO and co-founder of oXYGen Financial, a financial planning firm in Atlanta that caters to customers from generations X and Y.

“Like anyone who’s young, they’re 10-foot-tall and bulletproof,” he says.

But characteristics specific to millenials also might factor into Gen Y’s underinsurance, says Kit Yarrow, a financial psychologist at Golden Gate University in San Francisco, and author of “Gen BuY: How Teens, Tweens and Twenty-Somethings are Revolutionizing Retail.”

Millennials grew up with overprotective parents, which decreased their level of fear – and fear is what propels people to buy insurance, Yarrow says.

Gen Y: Underinsured and overconfident

Gen Y’s lack of insurance doesn’t stem from a lack of concern about finances, however. In the survey, 95 percent of millennials said their overall financial security is either very or somewhat important — almost exactly the same number as older consumers aged 30 to 64. But the survey revealed that not having enough insurance coverage could leave Gen Yers vulnerable to financial problems if a crisis hits. For example, the survey found:

- Only 64 percent of Americans age 18 to 29 have auto insurance, compared with an average of 84 percent for all older consumers.

- Only 10 percent of adults under 30 have homeowners insurance, while more than half of consumers ages 30 to 49 have it and 75 percent of those 65 and older do. A likely explanation: Fewer Gen Yers are buying houses and more are living at home with their parents, Lewis says. But only 12 percent of 18- to 29-year-olds have renters insurance despite the fact that almost four out of five adults under 25 live on their own, and two-thirds of adults ages 25 to 29, rent their homes, according to a report from the Joint Center for Housing Studies of Harvard University.

- Only 13 percent of consumers age 18 to 29 have disability insurance, compared with 37 percent of those 30 to 49.

- And only 36 percent of adults under 30 have life insurance, compared with 60 percent of 30 to 49-year-olds.

When millennials do buy insurance, they’re likely to get a bare-bones policy. In the survey, 36 percent of under-30 adults said they have only the minimum of any type of insurance required by law or a lender. In contrast, only 23 percent of adults ages 30 to 49 and 21 percent of those 50 to 64 said the same.

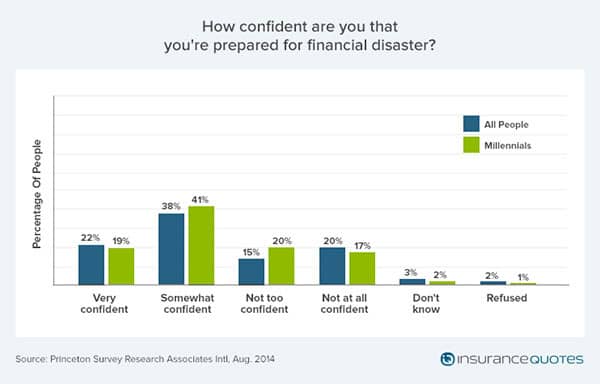

Given their underinsurance, Gen Y consumers appear to be overconfident in their ability to handle a life crisis.

In fact, 60 percent of millennials said they’re either very or somewhat confident they’re prepared for the potential financial impact of a life event such as a car accident, having belongings stolen, getting hit with substantial medical bills or becoming disabled.

In fact, Gen Yers had the most confidence of any group except for those 65 and older (68 percent).

“They tend to be a pretty optimistic crowd, and their view on money is that they’re going to be OK,” Yarrow says.

Millennials risk going without health insurance

However, it’s surprising how many millennials are going without health insurance, despite the Affordable Care Act’s requirement to buy it.

This may be because many Gen Y consumers are burdened with student debt that, in some cases, is the size of a mortgage, and many don’t think they need health insurance.

“If they get sick, they go to urgent care,” Lewis says.

Since millennials are active consumers of information, they might feel it’s unfair that they’re now required to get health insurance whether or not they think they need it.

“They understand they’re subsidizing older people and less healthy people through their good health,” Yarrow says.

But millennials should never go without health insurance; one serious accident or illness — or even a visit to the ER — can cause major money problems, says Sally McCarty, senior research faculty at the Georgetown University Health Policy Institute.

The median cost of a visit to the ER varies from $740 for an upper respiratory infection to $3,437 for a kidney stone, according to study published in 2013 in the peer-reviewed online journal PLOS ONE.

Open enrollment for Obamacare starts on Nov. 15, 2014, but you might qualify for a special enrollment period earlier if you’ve had a change in life circumstances such as having a baby, getting divorced and losing health insurance or moving outside your plan’s coverage area, according to HealthCare.gov.

Use the insuranceQuotes.com Obamacare subsidy calculator to see if you qualify for a subsidy on your premium.

Insurance tips for Gen Y consumers

Millennials might be underinsured partly due to misinformation, the survey shows. For example, the No. 1 reason (33 percent) consumers ages 18 to 29 gave for not having life insurance is that they can’t afford it.

The rate for a 25-year-old nonsmoking female in excellent health for a $250,000, 20-year-term life insurance policy could be less than $140 a year, or just over $11 a month.

Here are three insurance shopping tips for millennials.

1. Don’t assume it’s too expensive.

Shop around and get quotes because insurance might be more affordable than you think, says Jeremy Bowler, a senior director who leads the global insurance practice at J.D. Power, a market research company.

For example, the average renters insurance policy costs $10 to $30 a month, according to the National Association of Insurance Commissioners. “For the price, the coverage really is quite fantastic,” Bowler says.

2. Don’t always go for bare minimum coverage.

For example, buying only the mandatory state minimum amount of auto insurance can open you to financial risk if you were involved in a lawsuit.

Look for other ways to save, says Jamie Macgregor, a senior vice president for research consulting firm Celent, which conducted a panel on Gen Y and insurance.

For example, millennials should consider pay-as-you-drive insurance in which you install a tracking device on your car and get a discount for good driving.

It could be a good fit for younger consumers, who may be more willing than older consumers to be willing to share their driving data — especially when they get something in return, Macgregor says.

3. Don’t overestimate your invincibility.

Many Gen Y consumers say they don’t need life insurance, but they might, Lewis says.

For example, a young person with tens of thousands of dollars in student loan debt that Mom and Dad cosigned on might want to purchase life insurance, he says.

And many young consumers forgo disability insurance even though their biggest asset is the ability to earn an income, Lewis says.

Disability insurance replaces part of your income if you become disabled and can’t work. More than 1 in 4 of today’s 20-year-olds will become disabled before retirement, according to the Council for Disability Awareness, a nonprofit educational organization. Lewis recommends Gen Y consumers learn how disability insurance works and buy it.

View the press release here.

Methodology:

The PSRAI August 2014 Omnibus Week 1 obtained telephone interviews with a nationally representative sample of 1,003 adults living in the continental United States. Telephone interviews were conducted by landline and cellphone. The survey was conducted by Princeton Survey Research Associates International (PSRAI). Interviews were done in English and Spanish by Princeton Data Source from August 7 to 10, 2014. Statistical results are weighted to correct known demographic discrepancies. The margin of sampling error for the complete set of weighted data is ± 3.5 percentage points.

- About the Author

- Latest Posts

Lauren Pezzullo is an insurance content strategist and consumer trends analyst. She has led editorial teams at major brands and written for the Center for Health Communication at UT Austin. Her work covers home, auto, and health insurance topics.